Current Expected Credit Loss (CECL) Scenarios Service

Oxford Economics' solution for projecting expected credit losses to meet CECL accounting standards

Talk to us

What is CECL?

Our bespoke scenarios for CECL accounting

With over 35 years of independent forecasting and risk analysis experience, we are uniquely placed to assist companies with their CECL requirements. Our CECL scenarios service leverages our validated international and regional macroeconomic models and advanced risk-tracking tools to provide an unbiased view of potential upside and downside risks to the macroeconomic outlook and local forecasts for all 50 states and 382 metro areas of the United States and globally. By assigning clear probabilities to these outcomes, we offer precise scenario forecasts that reflect the current balance of risks, which clients can use when calculating their current expected credit losses under CECL.

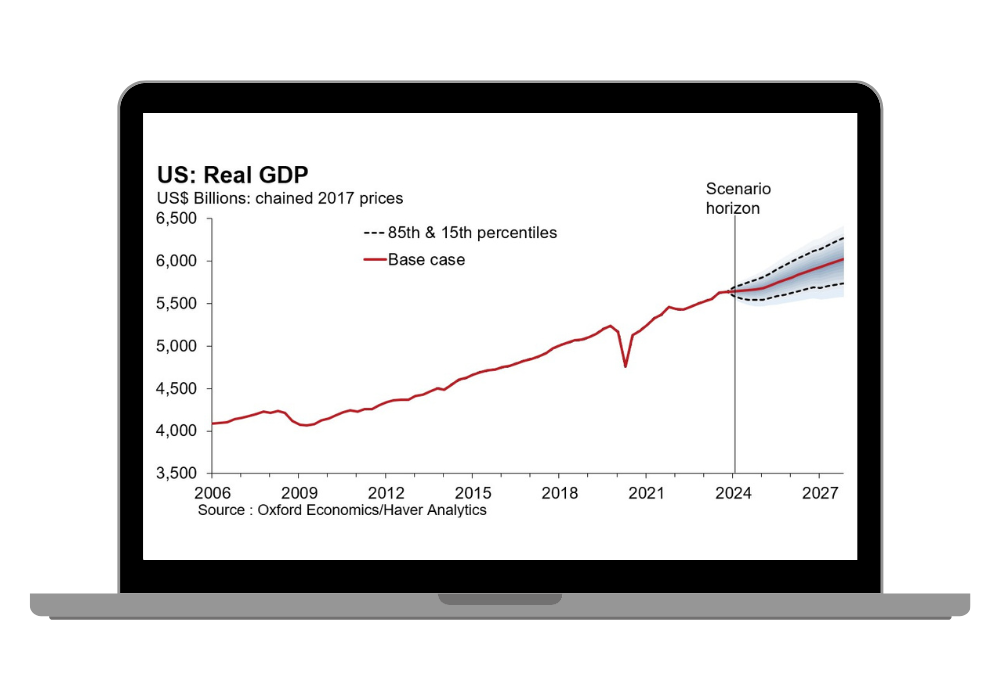

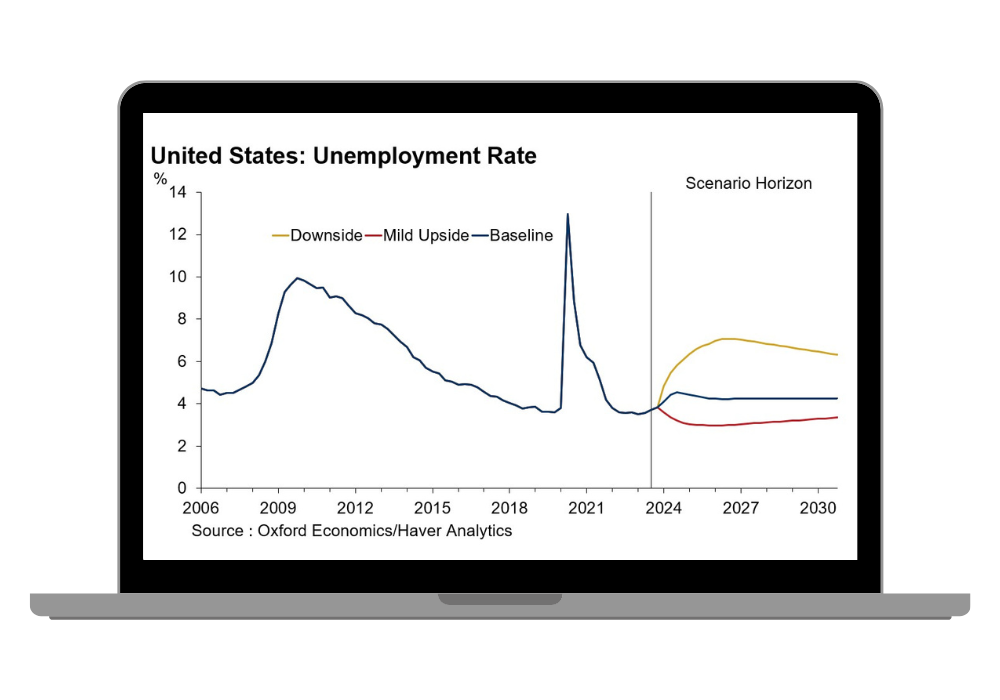

Baseline, upside and downside macroeconomic scenarios

We provide scenario results spanning the probability distribution of forecasts and covering the expected lifetime of assets. Our robust and internally consistent modelling capabilities allow us to cover international macroeconomic variables, as well as state and metro-level US impacts. Our Severe Downside CECL scenario is comparable in severity to the Federal Reserve’s Severe Adverse CCAR scenario.

Extensive reporting

The report accompanying our scenarios details changes in our baseline forecast against the previous update and movements in the balance of risk based on our analysis of current trends. We also provide a description of key topical risks, our scenario methodology and the impacts of the alternative scenarios on the US economy and financial markets.

Regular updates

To enable timely provision for credit losses, our CECL scenarios are updated quarterly to reflect emerging risks and changes to the base case. Subscribers to our wider offerings can also benefit from more regular updates to our baseline forecast and topical research briefings.

Comprehensive variable coverage

We provide macroeconomic and financial variable outputs that cover the key drivers of impairment. Fully consistent scenario results are available both at a national level and for all US States and Metropolitan Statistical Areas (MSAs).The CECL scenarios service you can trust

Why use macroeconomic scenarios for current expected credit loss calculations?

In the early years – when many were still asking, ‘what is CECL?’ – various approaches to meeting CECL accounting standards were adopted. Today, it is increasingly common to use multiple scenarios to assess expected credit losses. This CECL methodology allows institutions to incorporate a range of potential outcomes into their CECL calculations, ensuring that diverse risks are considered, rather than depending on a single forecast. With auditor approval and recent episodes of macroeconomic volatility, we anticipate this multi-scenario approach will become the industry standard.

For the baseline forecast – which has the highest probability attached – our clients benefit from our industry-leading forecasts, produced by a team of more than 400 full-time economists and analysts. Our commitment to quantitative rigour, combined with the calibre of our staff, consistently produces reliable results, as evidenced by our top multi-year rankings in various forecast accuracy surveys and business awards.

How do we construct our CECL scenarios?

CECL scenarios that everyone can understand

We know that CECL scenarios are used by a wide range of stakeholders, including non-specialists. As a result, we focus on providing transparency around scenario results, making them accessible and understandable for everyone from auditors and risk managers to broader internal stakeholders and the C-suite.

Alongside our data, we provide detailed reports that clearly outline the assumptions behind the baseline and scenarios. We also provide extensive ongoing support, including direct access to our production team for ad-hoc queries, assistance with auditor requests, and a dedicated account manager to field questions and connect you with our wider organisation where relevant.

“CMHC’s Stress Testing and ORSA team has started this year using Oxford Economics for the purpose of stress-testing. Our experience has been very positive. The software is sound, intuitive and user friendly. But most of all, it allows the user to understand the links between the variables and for a certain degree of customisation.”

“Services provided are always delivered timely according to the agreed timetable. Output is solid and in discussions OE has shown to be very responsive and proactive. Turnaround time is quick.”

“We wanted to bring our climate assumptions and scenarios more in line with those used by central banks in their climate stress test analysis, so we have worked with Oxford Economics to apply their climate macro model to our productivity, GDP and inflation forecasts. Oxford Economics has always been available to respond to our queries and provided insightful explanations for the impact of carbon pricing on macroeconomic activity in their model. We are very satisfied with their rigorous approach in modelling climate change and are happy to have collaborated with them.”

Resources and events

Financial markets

Takaichi’s big win doesn’t affect the fiscal outlook for Japan

Energy and commodities

2026 Winter Olympic medals: How metals prices reshaped medal values

Supply chains

Mapping the future of the UK industrial strategy: Sectoral and regional growth outlook

Economic growth

2026 Global economic outlook conference: Top questions on AI, trade, politics and growth

No events found.

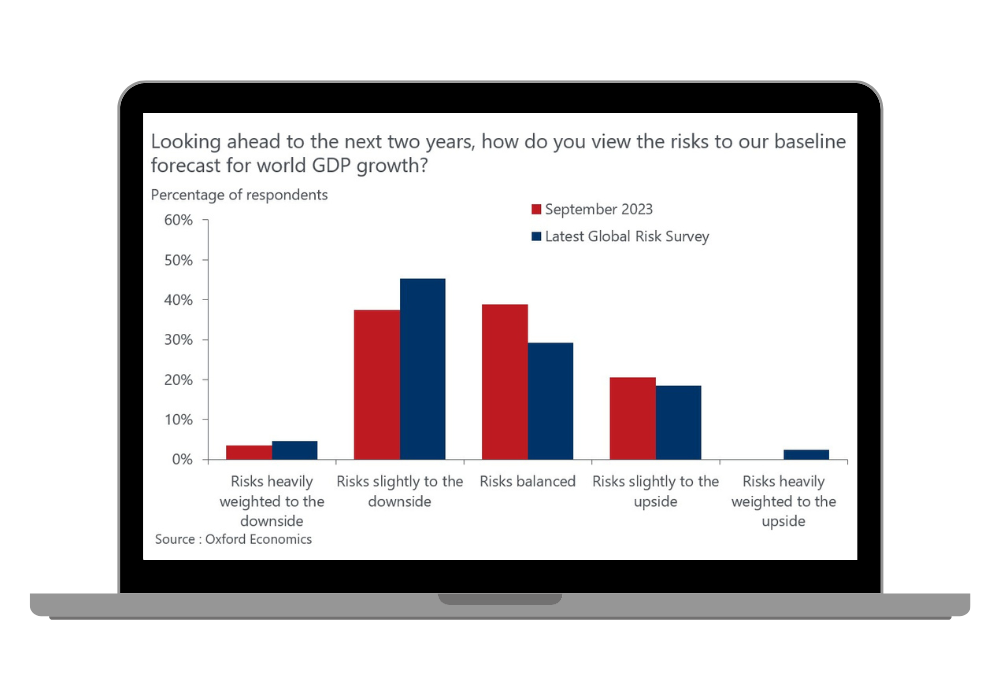

Greater downside risks are explored in our Q4 IFRS9 and CECL scenarios

Contact us

Trusted By

Please Add Form