COP 30 in focus: How to stay the course on the path to Net Zero

Ten years after COP21 and the landmark Paris agreement, COP30 is now drawing to a close in Belem, Brazil, the door to the Amazon rainforest, a macro-ecosystem threatened by mankind’s most daunting externality: climate change. And the challenge of climate change continues beyond COP30.

A decade on: progress toward net zero

Despite a decade of multilateral and national policy action under the framework of the agreement, the world remains on course for very substantial warming. The latest United Nations’ Emissions Gap Report points out that global emissions under current policies are likely to lead to 2.8°C of warming by the end of the century, well above the Paris agreement target.

What, then, has the Paris agreement achieved and what can countries now do to further bend the global emissions curve? To shed light on how best to move forward, let’s take a look back at the road travelled.

While it is impossible to know with certainty what the world’s emissions trajectory would have been without the Paris agreement, and the sceptics notwithstanding, it may not have been for nothing. The latest available estimates by the Climate Action Tracker suggest that it might have shaved off about 1°C of global warming (by end of century) compared to pre-Paris projections. Given the cost entailed by every degree of warming, such a change in the world’s projected emissions and temperature pathway is significant.

Nevertheless, the warming projected under current policies presents very severe risks to natural and human systems that warrant further action. Indeed, the best hedge against these low-probability but catastrophic events is to further reduce emissions. Hence the global community must redouble efforts to bring down global emissions at a scale and speed compatible with the goal of the agreement.

What, then, can be done?

At the current stage of the global transition, two levers of action have become clear: first, decarbonising heavy industry; second, enhancing advanced economies’ support for the decarbonisation of emerging market and developing economies (EMDEs).

Accelerating industrial decarbonisation

The decarbonisation of energy- and emission-intensive industry has been slow compared to other emitting sectors (e.g. power generation), even in countries or regions that have applied emissions reduction policies to them (e.g., the EU). This slow progress undermines the emissions reduction pathways of some countries, as the decarbonisation of other sectors is now well advanced.

Decarbonising industrial processes has long been seen as daunting. Many industrial sectors (e.g., steel, chemicals, cement) use fossil fuels as feedstocks or rely on very high-temperature processes that electricity cannot yet economically replace. Hence, as we highlighted in an earlier Research Briefing, there remain non-trivial technological barriers to industrial electrification or the replacement of these feedstocks by non GHG-emitting substitutes. Under current trends, we expect that industrial electrification will rise only modestly from 22% in 2021 to 31% by 2050.

Unlock exclusive climate and business insights—sign up for our newsletter today

Yet the decarbonisation of industry remains a necessary condition for the achievement of net zero targets. Given the substantial cost associated with the decarbonisation of industry, and the strategic importance to maintain an industrial base, emitting industries must receive adequate support. Higher carbon pricing, more competitive electricity costs, and targeted technology deployment support are essential to accelerate the deployment of emerging technologies such as plasma burners, electric arc furnaces, and green hydrogen.

Supporting low-carbon transitions in emerging markets

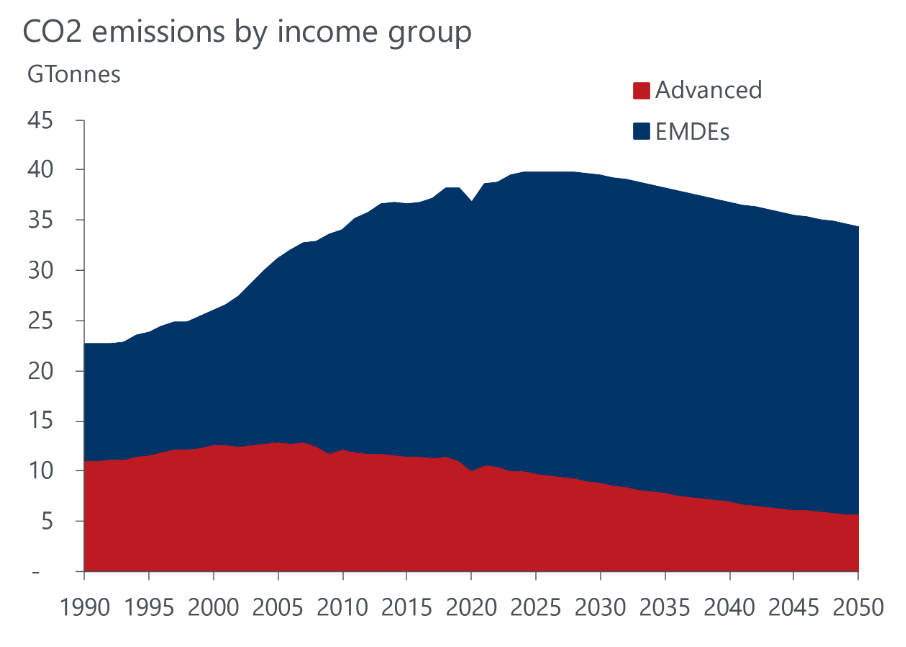

A second key to further reductions in global emissions lies in promptly helping EMDEs get on a low-carbon development path, as they are projected to release the bulk of 21st century emissions (Figure 1). The earlier these economies are steered toward low-carbon pathways, the more cumulative emissions are avoided, and the lower global temperature can get. This means extending the same emissions reduction pathways and technologies to EMDEs as those of advanced economies, including in industrial sectors.

Figure 1: Advanced economies represent an ever-shrinking share of global emissions

Given advanced economies’ historical responsibility for climate change and the speed at which global emissions need to come down, EMDEs’ transition should be adequately supported by advanced economies. This has long been acknowledged through the principle of common but differentiated responsibility enshrined in the UNFCCC and operationalised through a goal of USD 100 billion per year by 2020 agreed at COP15 in Copenhagen.

Most recently, this goal was revised to the mobilisation of USD 300 billion by 2035 under the New Collective Quantified Agreement reached at COP29. Alas, as was pointed out shortly after COP29, and as we discuss in this Research Briefing, the provisions of the agreement provide far too little resources in view of the African continent’s needs.

Our recent analysis suggests that, at the current level of domestic effort and international support, EMDEs reduce emissions too slowly, leading to modest reductions in global temperature by 2050 and negligible global benefits.

The conclusion is clear: advanced economies’ commitment to stabilising the Earth’s climate must increasingly translate into inducing emissions reductions beyond their borders.

Download our Research Briefings for a deeper dive

Advanced economy leadership is key to the low-carbon transition

Unlock climate financing for Africa

What will these changes mean for you and your business?

The next phase of climate action will move from pledges to implementation, reshaping markets, investment flows and competitiveness. Businesses that anticipate these shifts and quantify their exposure will be best positioned to thrive through the transition.

At Oxford Economics, we help you assess the impact of mitigation policies across every facet of your business. Request a trial of our Climate Services and gain access to forecasts, scenarios and expert insight, along with our latest updates from COP30 today.

Tags:

Related Reports

Key take-aways from COP30

COP 30’s agenda had placed a strong emphasis on countries’ implementation of their emissions reduction target and, for the first time, several workstreams included discussions on unilateral trade policies.

Find Out More

Flooding risks diverge across UK cities, sectors and economies

Climate-linked flooding is becoming more severe, reshaping risks for UK cities, real estate, and local economies. Which areas face the greatest impact—and why?

Find Out MoreAdvanced economy leadership is key to the low-carbon transition

We modelled how advanced-economy leadership in innovation and finance could accelerate a global low-carbon transition.

Find Out More

The changing energy order

To understand how the G20 countries are progressing in the energy transition, Oxford Economics PwC collaborated with PwC to create the Changing Energy Order Index. The index combines data from international economic organizations like the OECD and World Bank with with Oxford's own forecasts to evaluate each country's progress across five key pillars.

Find Out More