The Russia-Ukraine war: Three key dependencies affecting European industry

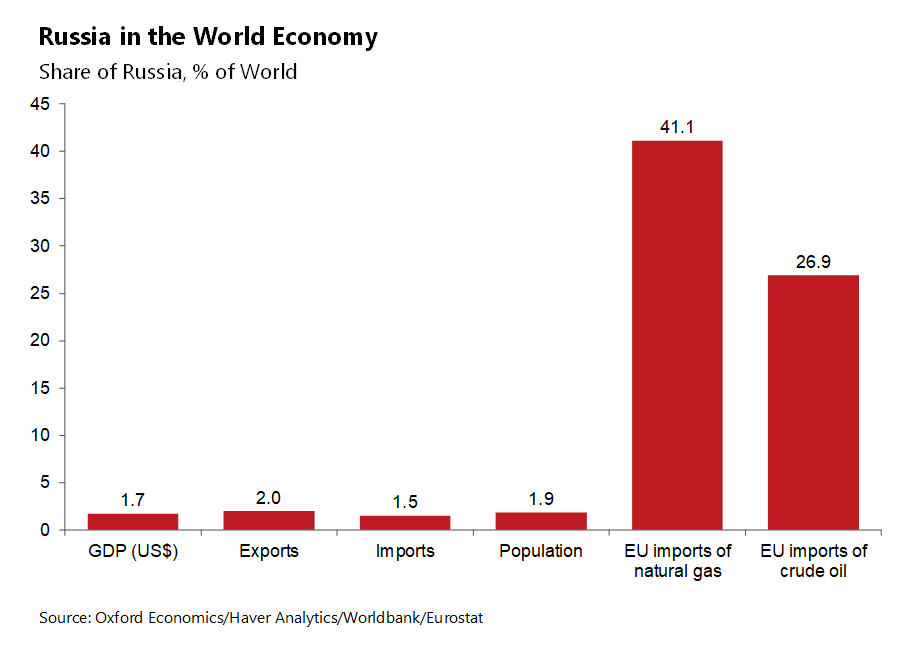

Russia’s huge oil and gas reserves, and the systemic importance of some commodities that are exported by Ukraine make the two countries a key part of the global supply chain. Europe in particular is heavily reliant on Russia for its energy needs, with 27% of EU total crude oil imports and 41% of total EU imports of natural gas coming from Russia (Chart 1). To understand how the Russia-Ukraine war might affect European industry, we have investigated three key channels through which the economic impact of the war will be felt.

Chart 1: Russia in the World Economy

- Dependency on Russian gas

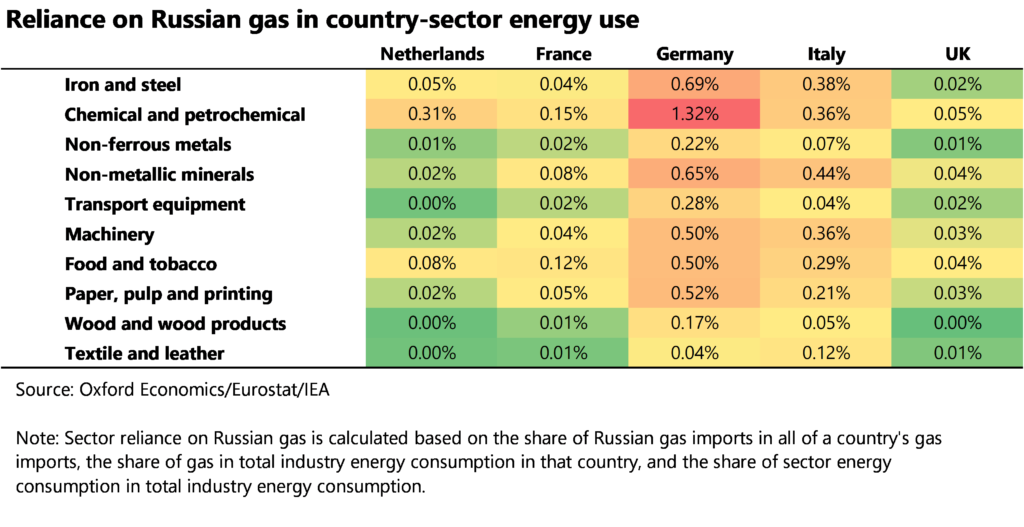

Immediately following the Russian invasion in late February, Brent oil prices reached their highest levels since 2014, while European natural gas prices skyrocketed. The negative impact on European industries is two-fold: Surging energy prices have caused inflation rates to climb to levels not seen in decades, squeezing real household incomes and hence consumption demand. Meanwhile, production costs have increased sharply. Table 1 aims to capture country-industry exposure to the latter. Sectors that are more energy-intensive (notably, iron and steel and chemicals production) and are located in countries with a stronger dependency on Russian gas imports (notably Germany and Italy) are likely to be more exposed to rising energy prices and changes in gas supplies by Russia.

Table 1: Reliance on Russian gas in country-sector energy use

- Dependency on Russian intermediate inputs

Following the invasion, the European Union, US, UK, Canada and other countries imposed a range of economic and financial sanctions on Russia that include export and import restrictions to and from Russia. Sectors with a strong direct dependency on Russian intermediate inputs are more likely to experience supply chain bottlenecks due to these sanctions or other logistics and transportation disruptions caused by the war. Table 2 shows that the dependence on Russia is concentrated in upstream sectors of the supply chain, reflecting the resource-intensive nature of European economies. The coke and refined petroleum producing sector stands out as the most vulnerable.

Table 2: Russian intermediate goods inputs as a share of total inputs

- Dependency on Ukrainian intermediate inputs

Similarly, sectors with a strong direct dependency on Ukrainian inputs are more likely to experience supply chain bottlenecks resulting from a drop in output of exported goods due to plummeting production and an inability to transport them. Table 3 shows that direct supply chain linkages between Europe and Ukraine are smaller than with Russia, but there are some potential pinch points—in particular, the European automotive sector shows the greatest degree of vulnerability. Although the share of intermediate inputs sourced from Ukraine is small in absolute terms, there seem to be very specific pockets within supply chains that have a higher exposure to the crisis. For instance, following the Russian invasion, German carmakers VW, Porsche, and BMW had to suspend production as war disrupted the supply of wire harnesses from Ukraine.

Table 3: Ukrainian intermediate goods inputs as a share of total inputs

While these pressures are not yet quantifiable, further disruptions brought about by firms’ inabilities to procure a specific part are likely to emerge over the coming months. The prospect of further sanctions and turmoil in commodity markets means that risks are heavily skewed to the downside.

Tags: