World Economic Prospects

Each month Oxford Economics’ team of 450 economists updates our baseline forecast for 200 countries using our Global Economic Model, the only fully integrated economic forecasting framework of its kind. Below is a summary of our analysis on the latest economic developments, and headline forecasts. To access the full report (and much more), request a free trial today.

Request a free trial

Lower oil prices aren’t a gamechanger for the growth outlook

- We’ve lowered our oil price forecast in response to the fragile truce between the US and Iran and the moderate pick-up in shipping traffic through the Strait of Hormuz. We’ve nudged up our 2026 world GDP growth estimate by 0.1ppt to 2.5%, and we’ve increased the 2027 growth forecast by 0.1ppt to 3.2%.

- The willingness of the US and Iran to negotiate is a positive step towards a lasting resolution. It reduces the risk of sustained closure of the Strait, making it less likely that a scenario plays out in which global oil inventories fall to critically low levels, triggering a damaging upward spike in the price of oil to reduce demand and align it with supply.

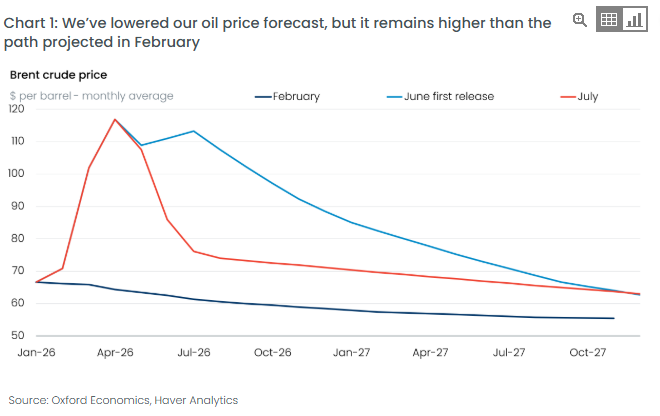

- We now expect the oil price will end this year at about US$70 per barrel, compared to US$87pb a month ago, and to fall to just above US$60pb by the end of 2027. While upside risks remain, a sharper easing of the oil price is also possible. Despite the revision, our oil price forecast remains above the path envisaged in February (Chart 1).

- Our lower oil price forecast has prompted us to revise down the Q3 peak in world CPI inflation by almost 0.5ppts compared to June and reduces the risk of second-round inflation effects. While weaker inflation will diminish the squeeze on households’ real incomes, we expect the activity boost to be limited – rather than buying more, many households may be less inclined to dip into savings to smooth spending.

- We’ve pushed back the timing of the next rate cut by the Federal Reserve to September 2027, reflecting the Fed’s focus on the inflation side of its mandate and upward inflationary pressures from AI. However, the case for hiking to prevent the oil price shocks leading to broader price pressures has lessened given the recent fall in the oil price. We think the bar to hike rates is high for both the Fed and other major central banks and we expect the next moves to be cuts.

Request a Free Trial

Complete the form below and we will contact you to set up your free trial. Please note that trials are only available for qualified users.

We are committed to protecting your right to privacy and ensuring the privacy and security of your personal information. We will not share your personal information with other individuals or organisations without your permission.

Find out how Oxford Economics can help you

Talk to us