Semiconductor downturn may be near a trough, but the near-term recovery is far from robust

After suffering an extended period of steep declines, we believe that the downturn in semiconductor sales may finally be nearing an end. The latest figures do show that the ongoing downturn in semiconductors deepened in early 2023. In April, the Semiconductor Industry Association reported global semiconductors fell 21.6% year-on-year, the steepest annual decline since the global financial crisis. The sector has been hit by a combination of weak end-use demand, a crash in cryptocurrency prices, new supply coming on stream, and inventory accumulation during the semiconductor shortage in 2021.

However, although end-use demand for traditional electronic goods such as PCs and smartphones remains weak, anecdotal evidence points to demand starting to pick up soon as computing devices bought during the pandemic are replaced. We have added semiconductor sales by region (for the Americas, Europe, Japan, China, Asia-Pacific, and World) in the latest update to our Global Industry Service. Our forecasts show global semiconductor sales reaching a trough in Q2 this year, before returning to growth in the second half of the year.

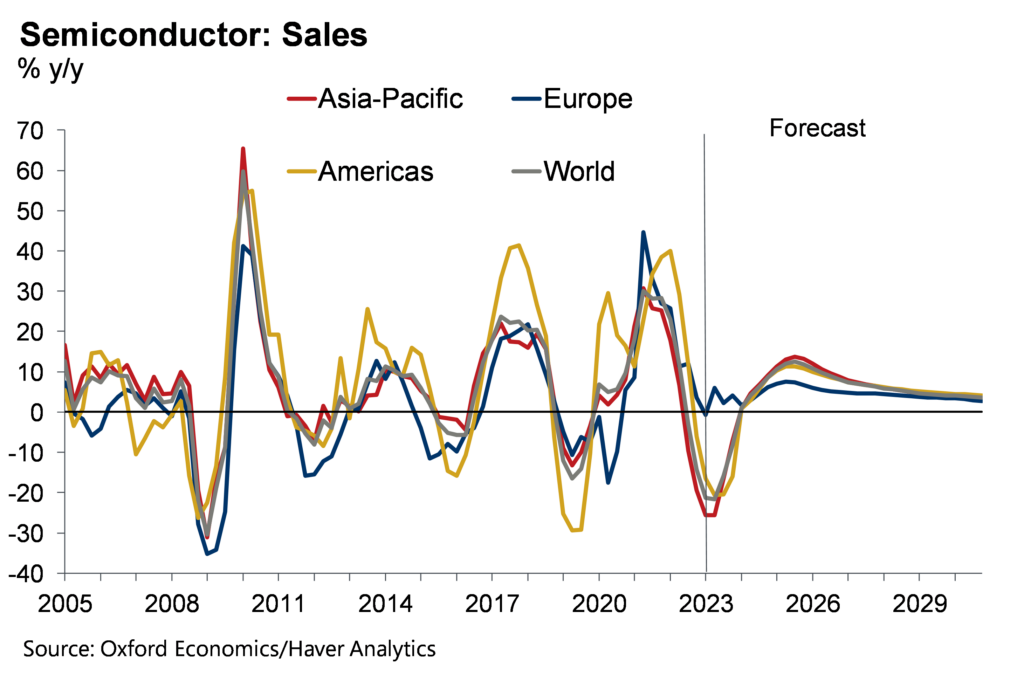

Nonetheless, we are unlikely to see a strong acceleration in growth in the near term. The inventory adjustment is taking longer than previously expected, according to TSMC, and the boost from the replacement cycle in electronic goods may be muted due to weak market demand. Moreover, the automotive sector—previously a bright spot for chipmakers—is likely to soften in the second half of this year. Overall, we expect a 16.9% decline in global semiconductor sales in 2023 with growth of just 5.1% in 2024 (see chart).

Medium-term outlook more robust

Despite the near-term slowdown, high-powered chips will be an important driver of manufacturing and productivity growth in the medium-term. Structural moves towards automation, the increase in the digital economy, and shifts in mobility and connectivity will drive continued demand chips. Already, Nvidia’s market capitalisation rose above $1 trillion on the success of its GPU chips used in AI computing, the A100 and its successor the H100, and going forward, high-powered chips will be key to driving the AI revolution. We expect global semiconductor sales growth to accelerate in 2025-2026 before settling near its average over the last decade of 5%-6% per year.

Author

Tags: