Research Briefing

| Dec 13, 2023

Industrial recovery on the way in the second half of next year

This year’s sluggish industrial momentum—the weakest annual growth outside of a major global recession since 2000—will likely carry over into H1 2024. While we believe interest rate hikes are mostly over, interest-sensitive sectors are being weighed down by the cumulative impact of past hikes, which combined with a weaker global economy is creating headwinds for industry.

What you will learn:

- EU industrial production has now declined for four consecutive quarters. Not only are energy intensive industries still depressed, but destocking and weak demand are increasingly taking a toll.

- While we continue to expect that US industrial output will shrink in Q4 and Q1 as interest sensitive sectors come under pressure and automotive production strikes create volatility, we now think the contraction will be very mild given the context of relatively robust consumer demand and our latest forecast that the economy as a whole will skirt a recession.

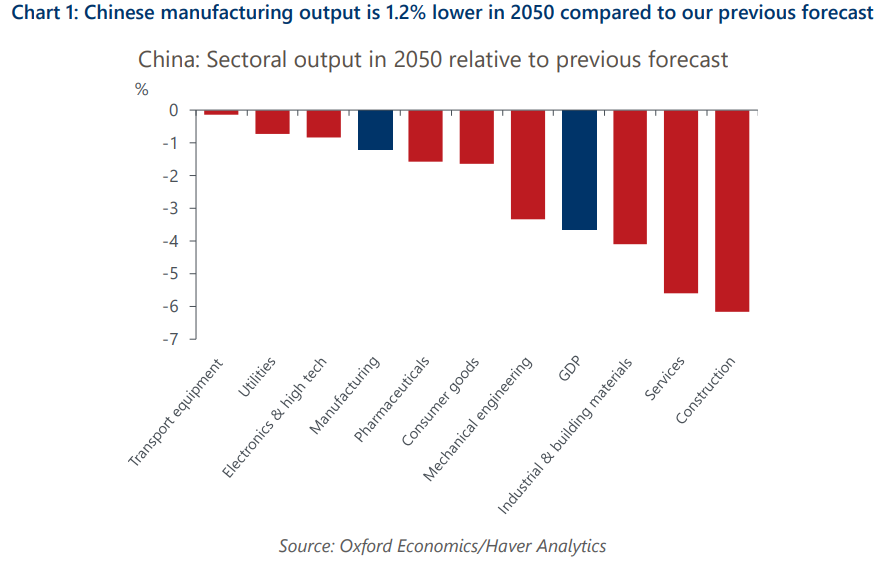

- We have downgraded our industrial growth forecast for China alongside our downgrade of GDP. The downgrades reflect our view that the residential construction and investment-led growth model is increasingly on the wane amidst overcapacity and the ongoing house price correction.

- China’s large proportion of total global industrial production (about 30% in 2022) has therefore caused a downward level shift to our long-term global industrial production forecast, which is now 0.8% lower by 2050 than previously.