We modelled how advanced-economy leadership in innovation and finance could accelerate a global low-carbon transition.

Yasuko Koido

Yasuko Koido

The Bank of Japan (BoJ) kept its policy rate at 0.5% at its October meeting, after a 7-2 majority vote. Two board members again voted for a rate increase. We believe the BoJ will hike in December to 0.75% as incoming data confirm that the economy is performing in line with the bank’s forecasts in its quarterly outlook. However, there’s a material chance of a delay.

We’ve brought forward the timing of the next Bank of Japan (BoJ) 25bps rate hike to December from next year and have added another 25bps hike in mid-2026. This reflects the surprisingly hawkish shift in the BoJ’s view since its September policy meeting and upward revisions to our growth and inflation projections, driven by the US economy’s resilience.

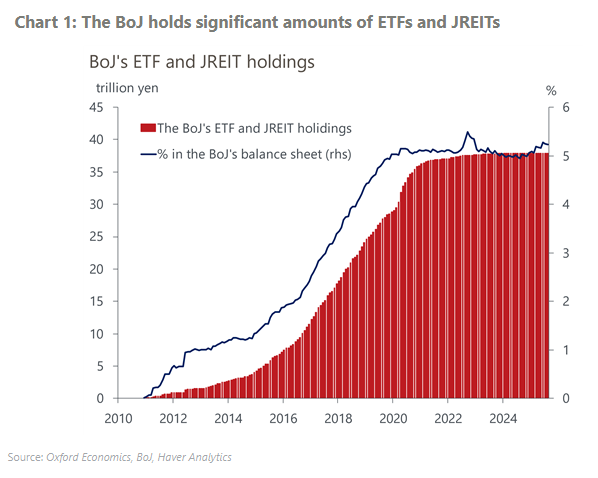

At its monetary policy meeting on Friday, the Bank of Japan (BoJ) unexpectedly announced it would start to sell its ETF and Japanese real estate investment trust (J-REIT) holdings. We think the impact of this plan on financial markets will likely be limited because the BoJ is opting to play it safe in terms of the process and the scale.

Research Briefing High uncertainty means a cautious the Bank of Japan

Software investment in Japan has risen sharply since the late 2010s, outpacing investment overall. We expect this high rate of growth to continue as the economy undergoes a digital transformation and the acute shortage of labour continues, driven by adverse demographics.

Japan, the world’s third-largest advertising market, is seeing a rapidly maturing online advertising sector, while traditional channels still account for roughly half of total ad spend. This presents significant opportunity for digital growth, and promises important benefits for small and medium-sized businesses and the broader Japanese economy.

We believe the huge increase in foreign workers in Japan will prove unsustainable, despite the considerable labour shortages across various sectors, caused by unfavourable demographics. As shown by the far right’s progress at the recent election, Japan isn’t ready to drastically transform policy and society to accommodate large numbers of foreign workers as full citizens, rather than as ‘guest workers’.

The Bank of Japan kept its policy rate at 0.5% at its July meeting. We continue to think the BoJ will exercise caution on rate hikes despite still-high inflation and a recent trade deal with the US.

We estimate that the US’s effective tariff rate on Japanese products is around 17%, in line with our baseline assumption. Lower tariffs on autos are a positive, given the sector’s significant contribution to the economy and its broad domestic supporting base

The ruling Liberal Democratic party (LDP) and its partner Komeito lost their majority in Japan’s upper house elections on July 20. Although Prime Minister Shigeru Ishiba will likely stay to avoid political gridlock, especially to complete tariff negotiations with the US, the political situation has become fluid and could lead to a leadership change or the reshuffling of the coalition.

Amid the continued decline in working-age population, we expect Japan’s knowledge-intensive manufacturing sectors will likely outperform other sectors. Machinery, automotive, and chemicals all require specialised know-how that are not easily replicable, and these sectors are striving to boost labour productivity through various forms of investment. The machinery sector will perform particularly well, with its share of manufacturing rising more than 1 ppt by 2035.

Our scenario analysis reveals a partial shutdown of the Strait of Hormuz by Iran would push the Japanese economy into a near-stagflation situation in H2 2025, given Japan’s structural vulnerability to terms of trade shocks.

The Bank of Japan kept its policy rate at 0.5% and announced its exit plan from quantitative easing at Tuesday’s meeting. Following a recent spike in ultra-long JGB yields, the BoJ decided to ease off the pace of reducing JGB purchases in FY2026.

We expect Japan’s fiscal outlook to deteriorate due to weak economic growth and pressure on the government to implement fiscal stimulus. We don’t think deficit concerns drove the recent spike in ultra-long Japanese government bond (JGB) yields, but as domestic purchasers reduce their JGB holdings, long-term yields could become more sensitive to fiscal developments in the coming quarters, raising the risk of a higher term premium.

During the recently concluded three-day Dragon Boat Festival in China, domestic tourism spending reached CNY42.7bn ($5.9bn), with a total of 119mn domestic trips made, rising nearly 6% year-on-year. While per-trip spending dipped, we caution against overinterpreting this single holiday, as travel has become more routine. Broader data points to a shift in Chinese household preferences away from goods and towards services such as tourism.

Japan’s industries, which are exposed more to international demand than to tepid domestic demand, are often concentrated in certain cities. This makes these cities more dynamic than others, a feature masked when only looking at national data. Understanding the industrial landscape helps identify growth opportunities across various sectors, as job creation and incomes drive spending.

The Bank of Japan kept its policy rate at 0.5% at Thursday’s meeting. Considering the significant downgrading of growth and inflation forecasts in its Quarterly Outlook Report, the central bank will likely take a long pause to assess the impact of high global trade policy uncertainty on growth and inflation.

We’ve cut our GDP growth forecasts for Japan by 0.2ppts to 0.8% in 2025 and by 0.4ppts to 0.2% in 2026, reflecting higher US tariffs and heightened global trade policy uncertainty. We now forecast that Japan’s economy will barely grow over 2025-2026 on a sequential basis.

US tariffs of 25% on all automobile and auto parts will weigh heavily on the Japanese and South Korean automotive sectors. A GTAP analysis suggests Japanese and South Korean automotive production will each shrink by approximately 7%. The impact is larger than suggested by bilateral trade data, because vehicles assembled in other countries before being shipped to the US will also be affected, dampening domestic auto parts production.