Assessing China’s revamped services sector

During the recently concluded three-day Dragon Boat Festival in China, domestic tourism spending reached CNY42.7bn ($5.9bn), with a total of 119mn domestic trips made, rising nearly 6% year-on-year. While per-trip spending dipped, we caution against overinterpreting this single holiday, as travel has become more routine. Broader data points to a shift in Chinese household preferences away from goods and towards services such as tourism.

New buzzwords such as ‘snow consumption’, ‘first-launch economy’, and ‘China-chic’ have amplified expectations around the unleashing of China’s services consumption potential. Policymakers increasingly view services consumption as critical in the context of the country’s slowing growth, especially amid rising external uncertainty and domestic structural weakness.

Since the mid-2000s, the share of China’s tertiary sector in GDP has risen by nearly 15ppts, approaching 60% in 2024. This structural shift has reshaped the labour market and mirrors the global trend of expanding services sectors as income levels rise.

Recent growth in China’s tertiary sector has been concentrated in household-oriented sectors, such as recreation and sports and tourism, alongside digitally accelerated distributive services such as retail and wholesale trade. In the short term, stimulating these sectors is likely to yield tangible benefits, especially for job creation and income stability.

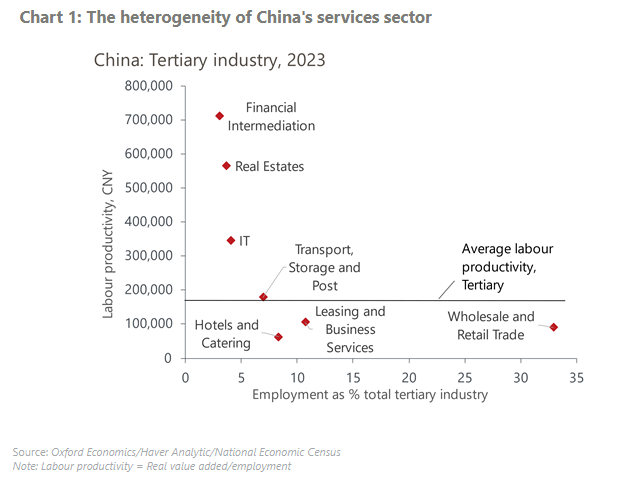

However, high value-added services, such as information technology, finance and logistics, have shown stronger productivity gains. Further integrating these segments into traditional industrial and services sectors will be increasingly vital for China’s productivity and supporting long-run economic transformation.