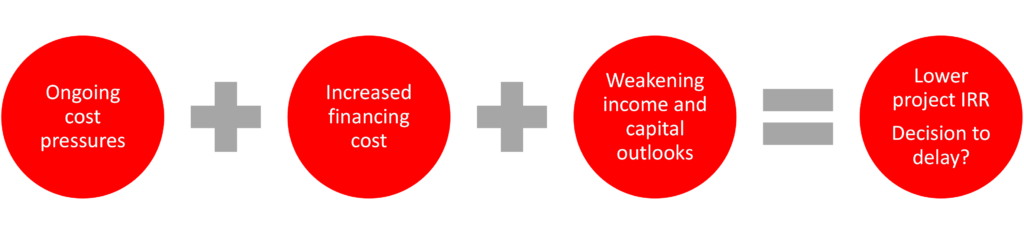

Multiple pressures to European real estate means infrastructure drive needs to be rethought

At the start of the summer we wrote about pressure on real estate development viability, as a range of factors combine to squeeze rates of return on capital to the point where some developments required unfeasible increases in rental or capital growth to remain viable. The months ahead will see difficult discussions being made around which developments should still go ahead in 2023. And policymakers need to ensure support for post-COVID recovery doesn’t make matters worse.

Figure 1 – Multiple pressures for real estate developers in 2023

The most visible component of the pressures facing developers is the rate of price inflation for construction activity through 2022. Construction costs have risen especially fast due to the sector’s energy intensity, but also due to shortages in materials and labour. October’s S&P Construction PMI survey found construction input price inflation was slowing as some bottlenecks eased. But in level terms costs are going to be appreciably higher going forward than anticipated earlier in 2022. Our latest forecasts indicate the cost of construction activity in key European markets in 2023 will be up to 10 % higher than in our pre-summer forecast.

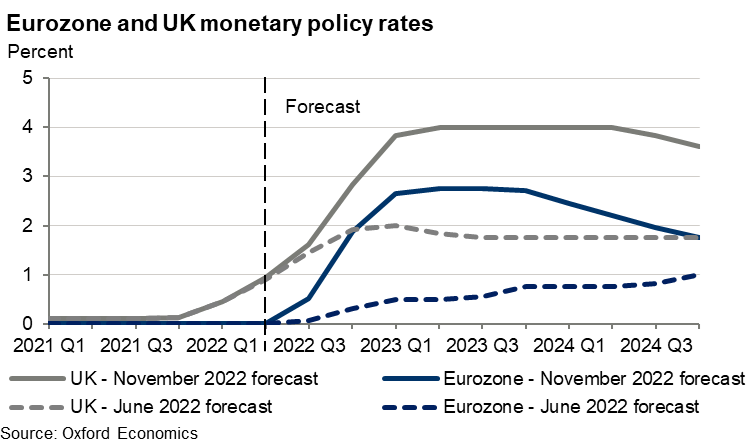

The cost of finance is also rising faster than anticipated a few months ago. In the eurozone, the ECB has signalled a much more rapid tightening of policy in the coming year, with rates expected to be 2% higher through 2023 and 2024 than anticipated a few months ago. Rates in the UK will also be around 2% higher through 2023 than previously expected as the Monetary Policy Committee focusses on protecting the credibility of its inflation target, even at the expense of growth.

On the demand side of the ledger, the combination of worsening price pressures, diminishing real incomes, and a tighter policy outlook mean the economic outlook has deteriorated further in the past couple of months. We revised down our expectation for UK GDP growth in 2023 by 1 percentage point between August and November forecasts, and now anticipate falling activity in the Eurozone late this year and early next. Across Europe the demand outlook for real estate has weakened, and with it developers’ pricing power for both rental and sales prices (especially in real terms). Our real estate service marked down our outlook for property returns substantially in our October release, and the likelihood is of worse price corrections to come.

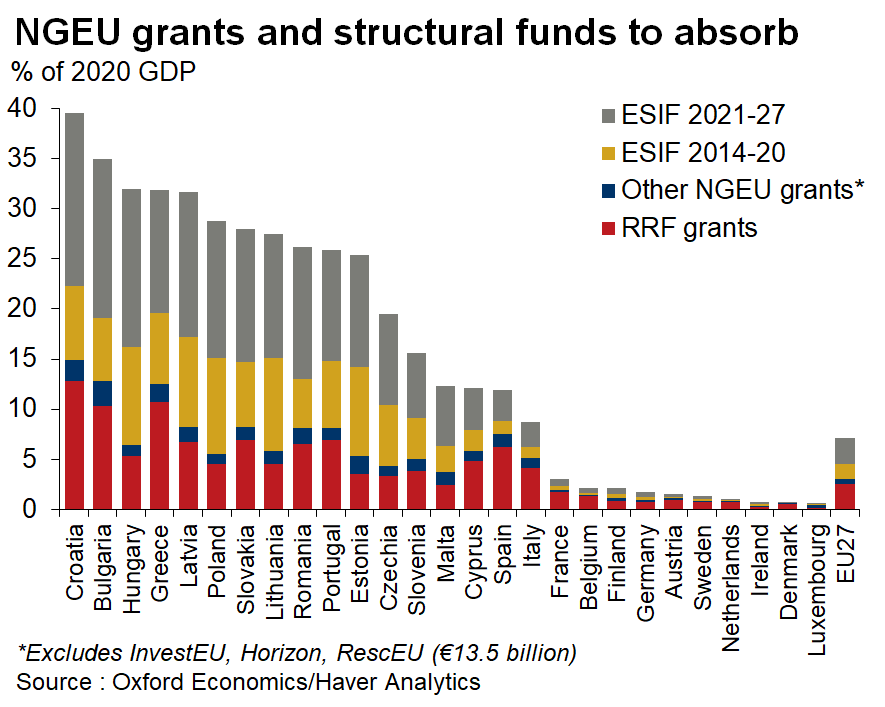

In the months ahead developers will be examining project finances to assess whether rates of return on projects remain viable in light of higher costs, dearer finance, and weakening demand. Some may decide construction needs to be put on hold until costs fall back further, or the economic outlook becomes more certain. And policymakers need to ensure that support for the post-COVID recovery doesn’t aggravate matters further. The EU’s Recovery and Resilience Fund (RRF) is heavily front-loaded in the coming couple of years and will boost demand for scarce construction resources – especially in countries where EU funds amount to 10% or more of GDP. There are plenty of measures the EU can take to ensure supply expands with capacity, but this may require a shift in mindset compared with the original goals of the RRF.

Note: ESIF = European Structural and Investment Funds, NGEU = NextGenerationEU, RRF = Recovery and Resilience Facility.

Author

Subscribe to receive latest real estate economics analysis

Tags: