Research Briefing

| Feb 11, 2025

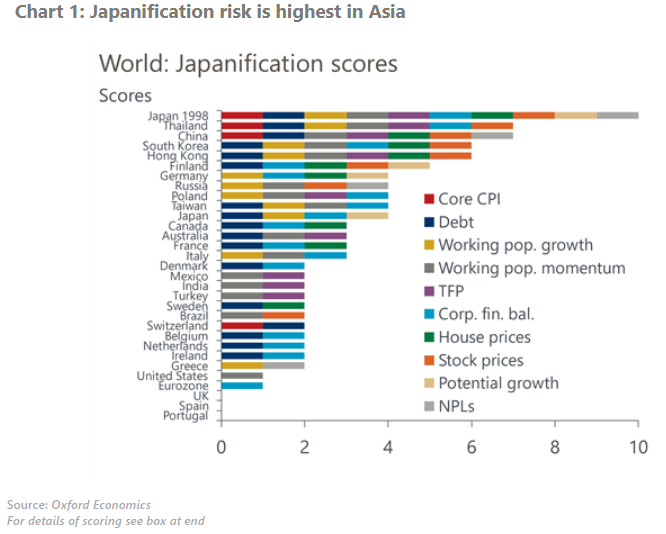

Japanification risk – down, but not out

Our updated analysis shows that the risk of ‘Japanification’ – a lengthy period of low growth and low inflation or deflation – has increased in Asian economies like China but declined in Europe. However, some of the changes may not be permanent. Economies are still settling down after the upheavals of the pandemic and some key underlying drivers of Japanification remain in place.

What you will learn:

- European risk of Japanification has declined due to a mixture of factors. Stimulatory fiscal and monetary policies during the pandemic broke the deflationary cycle, short-run trends in working population growth have improved, and bank and private sector balance sheets are healthier. But there are some exceptions to this pattern, most notably Germany, where Japanification risk is up.

- On the other hand, China’s risk of Japanification has increased due to a large and ongoing property sector decline, policies encouraging excess supply, and very low inflation rates. Symptoms of a balance sheet recession, like that seen in Japan in the 1990s and 2000s, are becoming visible. Other parts of Asia, such as Thailand, are showing similar trends.

- A key factor that could contribute to rising Japanification risk in the years ahead is demographics, especially for Asia. Unlike some other observers, we do not view ageing societies as an inflationary factor. In addition, weak potential output growth and continued excess corporate savings could raise Japanification risk.

- Overall, our measure of Japanification risk has declined across economies on average since 2019. However, this has arguably occurred mostly due to luck than design and has relied in part on the short-term impact of the aggressive stimulus policies of 2020-2021. A return to more restrictive policy settings in areas like Europe could cause the reversal of the recent improvement in Japanification risk.