Japan increased cost pass-through suggests prolonged high inflation

We have raised our CPI forecast for Japan for this year and next, reflecting a revised profile for oil prices. We now expect core-core CPI (excluding fresh foods and energy) will stay elevated for an extended period, falling to 2% only in Q4 2027, instead of Q2 2026 as expected two months ago.

Compared with 2022, cost pressures from import prices are likely to be milder. We expect the rise in oil prices in y/y terms to be smaller than in 2022, and we assume supply chain stress will be contained this time. The yen exchange rate, which amplified import inflation in 2022, is also likely to have a smaller impact on the import prices in our baseline.

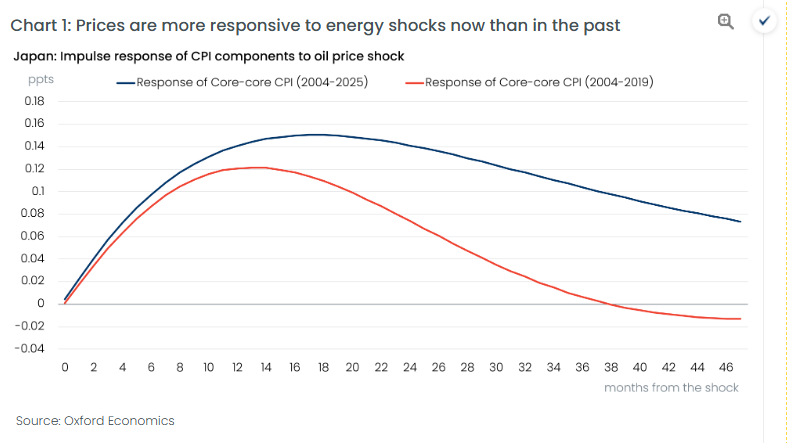

However, we think the pass-through of costs to final prices has been increasing since 2022, reflecting proactive pricing behaviour by firms. As a result, we think high inflation will persist for a lengthy period –depending on firms’ pricing strategies, it could continue for even longer.

We don’t think a wage-price spiral will be triggered. The 2026 spring wage negotiation is now being finalised, and the implied monthly wage growth is likely to fall short of inflation. High inflation in 2026 will push up the pay rises demanded in 2027, but increasing numbers of firms, particularly SMEs, will struggle to keep up with the rapid surge in wage bills as high oil prices simultaneously hit profits.

Despite a spike in CPI, we think inflation expectations are likely to stay anchored at around 2%, which will eventually bring down inflation in late 2027. Inflation expectation measures remained below 2% during previous periods of high inflation in 2022 and 2025.