Impact of the Iran-Israel escalation on oil prices

The military escalation between Israel and Iran has renewed fears of a major Middle East conflict, with significant implications for oil markets and the global economic outlook.

Israel’s latest strike directly targeted a key Iranian nuclear facility, while Iranian missiles hit an Israeli hospital, a stark shift in scale from earlier tit-for-tat exchanges. Although a full-blown supply-side oil shock has so far been avoided, the risk is clearly rising. The Brent crude oil price spiked by over 10% as the conflict started and remains elevated in the $70-$78 per barrel range at the time of writing, well above pre-escalation levels.

We’ve modelled three oil supply shock scenarios in our Global Economic Model.

Sign up to our webinar here: GCC Outlook: Will geopolitical tensions and tariffs offset domestic resilience?

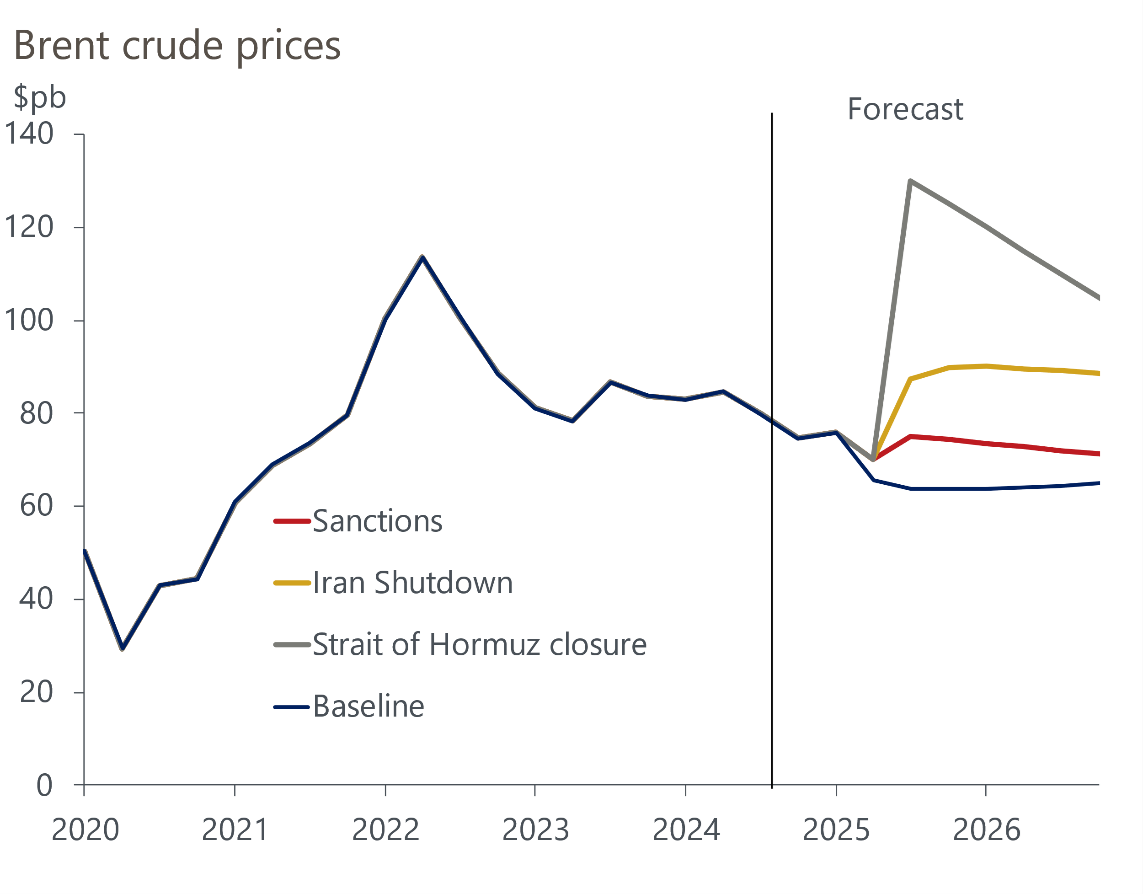

Chart 1: Oil supply shock scenarios versus our baseline forecast

Sanctions escalation (mild shock)

In the most benign scenario, Israel’s demonstration of its military reach and Iran’s controlled response create space for a quiet return to mutual deterrence. However, even this outcome could result in the West imposing tougher sanctions on Iran, leading to Iranian oil production decreasing by about 1% of global supply. Brent would likely remain at around $75 per barrel, roughly $6 above our current forecast, keeping global inflation marginally higher for longer.

Full Iranian export shutdown (moderate shock)

If the tit-for-tat attacks continue and Iranian oil exports cease, there would be a 4% reduction in global oil supply, with Brent likely settling closer to $90 per barrel through 2026. Global growth would take a mild hit – our models suggest a 0.2 percentage points downgrade to global GDP – but the real pain would be felt in higher inflation. US inflation could rise to 4.5%, potentially delaying interest rate decreases from the US Federal Reserve into 2026.

Closure of the Strait of Hormuz (severe shock)

The most severe scenario is a closure of the Strait of Hormuz. Around one-third of all seaborne oil passes through this chokepoint, and a shutdown would freeze oil exports from Kuwait and Qatar, and restrict exports from Iraq, the UAE, Oman, and Saudi Arabia. We assume this would lift Brent to $130 per barrel. Inflation could touch 6% in the US, and nearly 4% in the Eurozone. Although central banks might resist raising interest rates, they’d almost certainly choose to delay cuts, derailing hopes of monetary policy easing this year.

The conflict adds another layer of fragility to the global macroeconomic environment, with any meaningful deterioration in oil supply conditions pushing inflation higher, weakening real incomes, and altering the timing and magnitude of monetary easing in major economies.

In our most adverse scenario, world GDP would be about 0.3% below our current baseline in 2026, reducing GDP growth by 0.1 of a percentage point in 2025 and in 2026. The hit to economic activity would be slightly larger for the US and Eurozone, with GDP growth at 0.4% and 0.5% below our baseline forecasts next year, respectively.

For latest reports on the middle east, please visit our regional page.

Subscribe to our newsletters

Tags: