How 2025 reshaped long-run global economic risks

The past year has seen a reshaping of long-run risks, with rising trade uncertainty, threats of US isolationism, and accelerating AI investment. This is highlighted by our Global Risk Survey, which captures what clients perceive as key risks and informs how we update our Megatrends Scenarios.

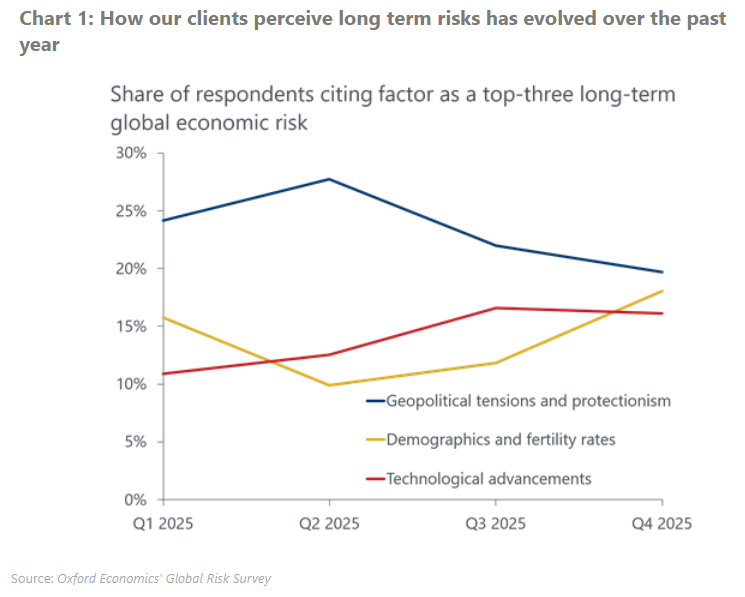

Trump’s ‘liberation day’ tariffs accelerated the retreat from globalisation. By Q2 2025, over one-third of businesses cited geopolitics and protectionism as the key long-term downside risk, prompting our baseline to move closer to our Fractured World scenario. The same America First shift also heightened client concern around institutional risk in Q4, which we assess in our Global Rebalance scenario.

Demographic change has also risen up the risk agenda, with 40% of clients citing it as a top concern at the end of last year, up from 25% in Q2. In our Secular Stagnation scenario, we show how weaker than expected fertility rates could constrain long-run output growth. Moreover, our forthcoming Zero Migration scenario will allow clients to assess how sensitive growth outcomes are to future policy choices.

Meanwhile, AI has emerged as the clearest source of long-run upside potential. Over half of respondents cited technology as a key upside risk in Q1 2026. This mirrors recent events, with US investment in information processing equipment and software growing at a 20%-40% annualised pace in early 2025, and adoption rates running higher than expected in the US.

Our new Tech Acceleration scenario assumes sustained high AI adoption in advanced economies, reinforced by successive waves of innovation that lift productivity growth structurally above baseline. Advanced economies benefit most, reflecting earlier deployment and greater readiness. Output growth increasingly outpaces employment, with US labour productivity rising at rates comparable to the early 1990s and significantly above baseline.