Why we expect JGB yields to stay high

We’ve raised our end-2026 10-year Japanese government bond (JGB) yield forecast to 2.8% from 2.5%. The prospect of higher inflation will keep yields elevated globally, and concerns about Japan’s fiscal expansion will also persist. We now see the risks to our JGB forecast as more balanced, although a further increase still isn’t out of the question.

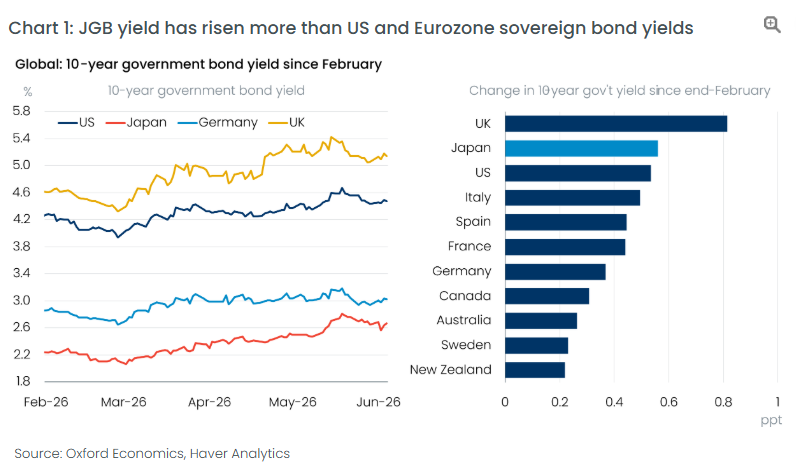

The 10-year JGB yield is around 2.7%, having risen sharply from 2.1% in March, fuelled by market concern about Japan’s more aggressive fiscal stance, in addition to the global repricing of yields driven by real rates and rising inflation expectations. The recent slight retreat in the 10-year yield can be attributed to June’s supplementary budget being smaller than markets anticipated.

The list of expansionary fiscal projects is quickly growing. The proposed cut to value-added tax (VAT) on food would have a significant impact on the fiscal balance in the absence of counterbalancing measures. Additionally, the government has proposed issuing “bridging bonds” to increase strategic investment. The policy direction should become clearer by around the end of June, and we may need to revise our forecasts accordingly.

The combination of the slow rise in the effective interest rate cost and strong tax revenue driven by inflation and solid growth means Takaichi can stick to her ambitious fiscal promises. Even with our new yield forecast, we don’t think the government debt-to-GDP ratio will start to rise until mid-2027, and then only gradually, thanks to the large stock of JGBs issued at times of low yields.