What we know about private credit risks

Rising risks in private credit are unlikely to trigger systemic fallout, but pockets of vulnerability remain

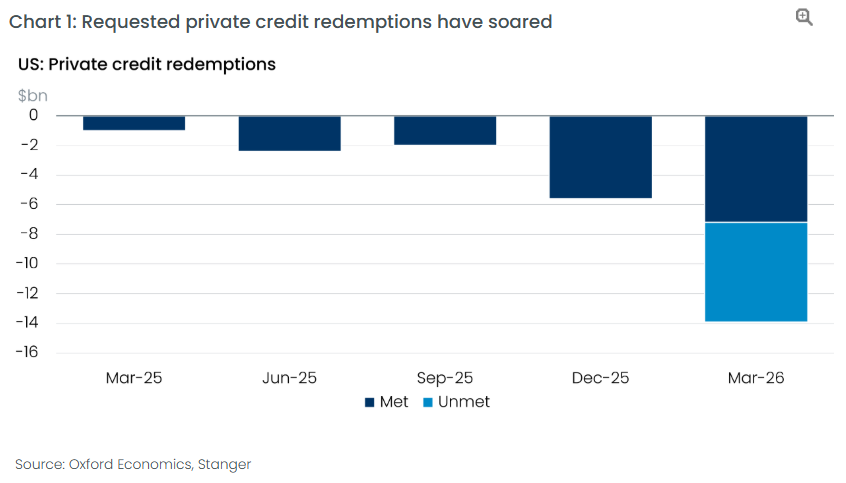

Recent stresses in the private credit market reflect very real problems in the sector, but we don’t think there is a major risk to financial and economic stability. That would require problems in the private credit sphere to spill over substantially into broader public credit markets, which we think looks unlikely.

The private credit market remains small at less than 3% of total US private debt. This doesn’t preclude a systemic threat, as the subprime mortgage market was of a comparable size in 2006. It was massive spillovers from subprime to other credit segments that eventually triggered the global financial crisis (GFC).

Other similarities with subprime that are stoking concerns include evidence of loose underwriting standards and the ‘repackaging’ of weak credits.

Overall, however, we don’t think major spillovers from the private credit market are likely this time. Unlike the period prior to the GFC, we are not in a major credit boom. In fact, US private sector leverage has been declining in recent years.

That said, there is scope for some unpleasant repercussions. Banks’ exposure to private credit looks moderate at around US$300bn, but their exposure to other non-bank financial institutions is an additional $2tn and has been rising quickly. Insurers, whose exposure to private credit is around $1tn, could also suffer negative consequences, although the impact would be likely to be more of a slow burn.

Download the report to learn more.