What Does “Normal” Look Like for the GCC After the Middle East Regional Conflict?

Oxford Economics expects GCC activity to rebound within 1–2 years after a peace agreement. Though investment, tourism and capital flows may take longer to recover.

One question came up repeatedly during my recent panel discussion on the Gulf economy: when will the GCC feel ‘normal’ again? The Middle East conflict recently passed a 100-day mark, although the region has been in a period of relative stability for some time. As the US-Iran peace agreement takes shape and activity in the Straits of Hormuz gradually normalises, the more interesting question is what “normal” looks like — and how long it takes to get there.

By normalisation, we mean a return to pre-conflict trends in growth, investment, and capital flows. Our base case is roughly one to two years from a definitive end to the conflict, though the path will be uneven across activity, confidence and capital.

Activity rebounds first

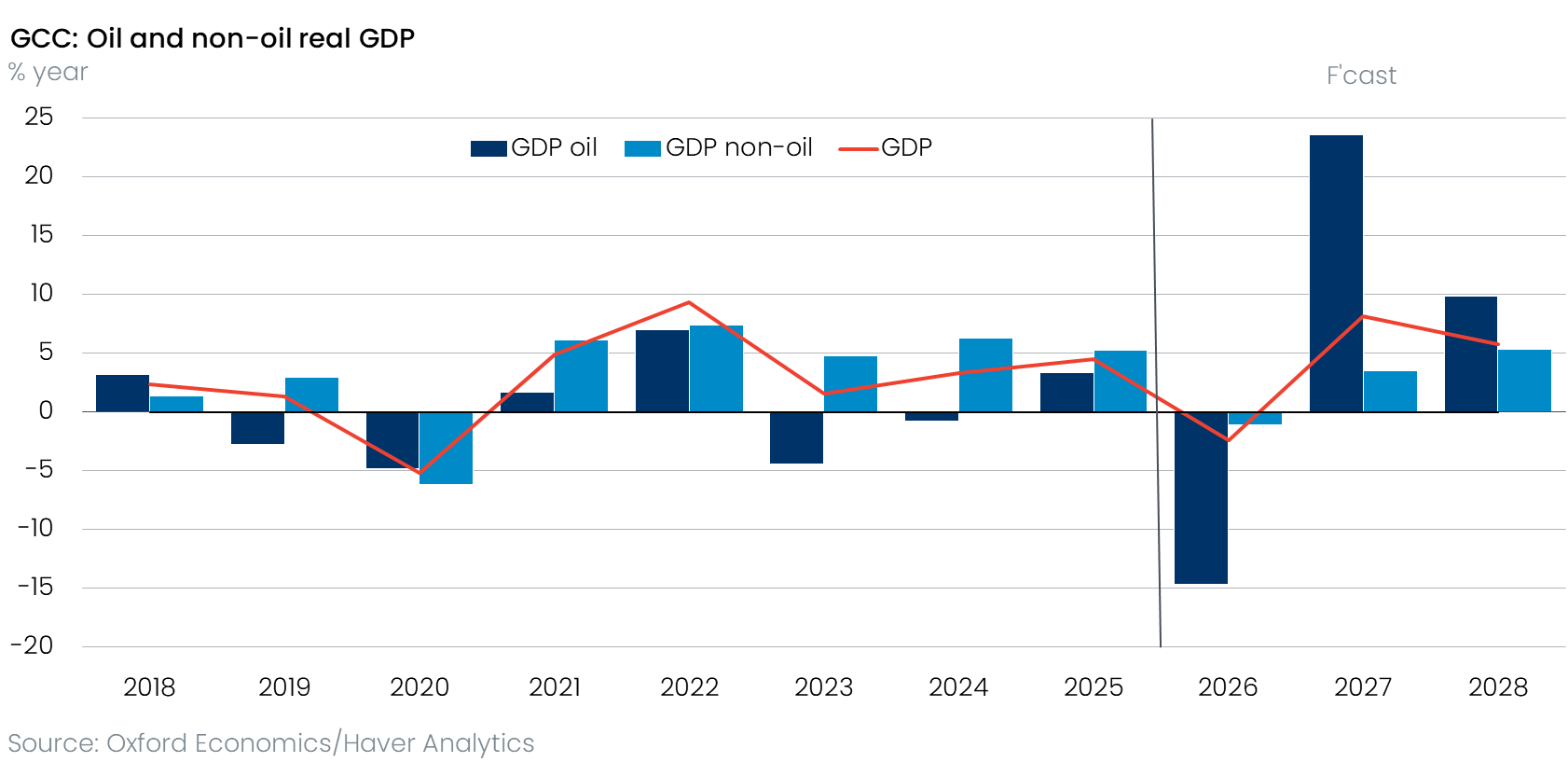

Day-to-day economic activity should recover relatively quickly. Much of what has been disrupted — cross-border trade and tourism — can be restarted once the geopolitical picture clears. However, the picture will vary across sectors: oil production will normalise quickly once the Strait of Hormuz fully opens. Similar, manufacturing and construction follow a similar shape: imports of materials and access to export markets have been disrupted, and the rebound will be sharp but staggered.

Saudi Arabia and the UAE still have significant fiscal space and sovereign wealth firepower to smooth the cycle through public investment. We expect them to use it and this will support domestic activity.

Some sectors, however, are likely to experience a longer recovery tail. Tourism arrivals are tracking a roughly 39% decline this year, reflecting a deterioration in confidence amid conflict-related disruptions, followed by around 42% recovery in 2027 and a return to 2025 levels by 2028. That cycle will spill into tourism-dependent sectors and matters disproportionately for non-oil growth in a number of GCC countries.

Confidence and capital lag

Confidence is slower-moving and more uncertain. Households and firms will stay cautious for some time and international investors longer still. Capital flows typically lag the real economy by several quarters once a clear political settlement is in place; absent that clarity, risk premiums stay elevated even as activity normalises.

The headline, then: activity in a year or two with some sectors normalising more quickly, with confidence and international capital flows recovering too but lagging a little behind in the return to normality.

A cyclical shock with structural echoes

Is the conflict a short-term cyclical shock or a hit to the region’s growth model? Honestly, a bit of both. Structurally, higher risk premiums on capital, higher insurance and logistics costs, and the need to diversify trade routes will weigh on confidence and the cost of doing business. There is also a demographic dimension: the GCC’s growth model rests on an expat-heavy labour force, and if wages have to rise to attract migrant talent and entrepreneurs, this would be an additional headwind.

Opportunities on the other side

The fundamentals that drove pre-conflict performance haven’t gone away — notably business-friendly reforms and policy ambition with transformation agendas backed with large scale capital deployment. This is particularly the case in the UAE and increasingly Saudi Arabia.

On AI, for example, the GCC remains particularly well-positioned still, with low-cost power, capital to deploy and a willingness to move quickly on data-centre infrastructure.

Higher public and SWF investment in local diversification to achieve objectives such as reducing import dependence to improve food and water security and enhancing logistics that scale back dependency on the Straits of Hormuz — pipelines, ports, rail networks — could all become additional tailwinds. Higher defence spending will add to growth too.

Final thoughts

The GCC will return to being one of the strongest-performing regions in the world economy, with some ongoing headwinds but also new catalysts that didn’t exist before. Not a worse economy — perhaps a slightly different one.

You might also be interested in

Subscribe to our newsletters

Sign up to our newsletter to download the latest and most popular reports.

SubscribeWhat does the GCC’s new normal mean for your organisation?

Whether you’re assessing investment opportunities, planning market entry, or evaluating economic risks, our Macro Consulting team can help. Get in touch to start the conversation.