Rough road ahead for US Construction under Trump 2.0

The construction sector has experienced wild ups and downs in recent years, a trend that looks set to continue under the next US administration. In the short term, fiscal stimulus will lead to stronger investment growth, benefiting non-residential construction. However, by the end of the decade, the construction sector will face significant headwinds due to President-elect Trump’s polices on immigration and trade, eventually leading to higher input and borrowing costs for the sector.

Fiscal policy to boost construction in the short term

We expect President-elect Trump to extend the 2017 Tax Cuts and Jobs Act (TCJA) and the expiring personal tax provisions. The expansionary fiscal policy will likely result in a short-term increase in business demand, supporting a higher level of investment spending. However, our baseline assumes that the long-term risks associated with higher tariffs and immigration cuts will dominate in the out-years.

There’s also been commentary around Trump’s desire to cut spending associated with the IRA and CHIPS acts. We assume in our baseline that the clean energy tax credits within the IRA will be preserved as multiple Republicans are on record supporting the credits and many red states have disproportionately benefited—a boost for our construction outlook. The total suite of policies presents an upside risk to inflation and are likely to lead to interest rates remaining higher for longer (a risk that’s already playing out in higher mortgage rates). This could hamper private investment in construction projects, particularly in residential and large commercial projects.

Substantial long-term risks to construction growth

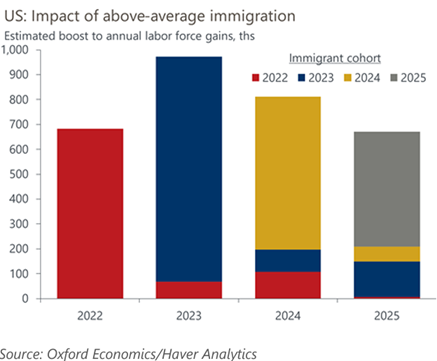

Repeated suggestions that Trump is serious about curtailing immigration spell trouble for the construction industry. Our baseline assumes that starting from mid-2025, net migration will fall from 1.1 million per annum to around 800,000 per year.

There are downside risks to this forecast as Trump has repeatedly threatened mass deportations, but we do not include this in our baseline. According to US census bureau data, 26% of construction workers are immigrants and 13% of workers are unauthorized, the largest share of any sector. A reduction in the labor force will exacerbate the labor supply issue that the sector already faces, raising construction wages and increasing cost inflation.

Unlock exclusive economic and business insights—sign up for our newsletter today

This will take time to manifest, however, as previous US arrivals will support the sector and the inflationary impact of costs will be lagged. The result of this is borne out in Chart 1; as new immigrants typically don’t join the labor force as soon as they enter the country, the impact of immigrations cuts on labor force gains won’t be felt until 2026 and beyond.

Tariffs form a key pillar of President-elect Trump’s economic policies and are likely to lead to higher input costs for the construction sector. In essence a sales tax paid by consumers, construction companies are likely to see the price for inputs such as lumber and steel increase as soon as the tariffs come into effect. There is some debate surrounding just how soon these tariffs can be implemented, but some will certainly begin to take effect by early 2026. Companies will face either a hit to profit margins, causing supply-side issues as businesses find less profitable work available, or they will be forced to raise prices. We may see firms try to shore up supplies or find new sources before tariffs come into effect, but this will also raise short-term costs as inventory expenses are high and nearshoring attempts seen during the initial US-China trade war are off the table due to likely tariffs on Canada and Mexico. Our baseline forecast assumes 10% tariffs on Canadian steel, aluminum, and base metals, with 10% on Mexican steel and aluminum as well.

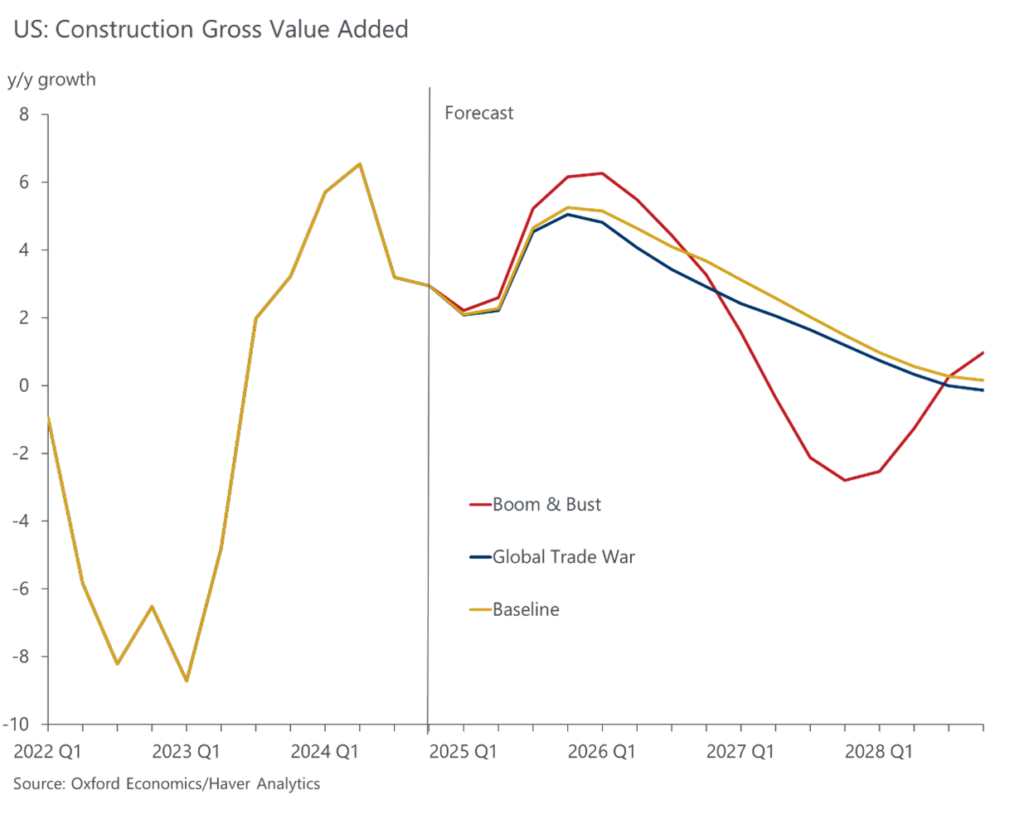

Beyond this, we’ve also run multiple scenarios via our Global Industry Model, including US Boom & Bust, to reflect the potential inflation concerns driving up market interest rates and overheating US economy due to extra fiscal stimulus. The Global Trade War scenario, on the other hand, simulates higher tariffs holding back trade growth while immigration curbs exacerbate US price pressures. Chart 2 highlights the impact of both on construction.

Chart 2. Trump’s announced additional tariffs could dampen economic results

The outlook for construction is riddled with uncertainty and contains many downsides risks. It remains to be seen whether the Trump administration will consider the long-term vulnerability of the sector when implementing his new economic agenda. We discuss these impacts and more in our latest industry highlight and the impacts are incorporated into the most recent updates of our Global Industry Service, the US Construction Service, and Global Construction Service.

To learn more about our December industry forecasts and how we factor in the influence of Trump 2.0 policies, download our report.

To discover how we can support you to navigate uncertainty with confidence, request a free trial.

Subscribe to our newsletters

Tags: