Inflation and stagflation in Oxford Economics’ IFRS 9 and CECL Scenarios

By Marc Pacitti

Conflict-related commodity price shocks and supply chain disruptions due to volatile trade policy have raised the salience of persistently higher inflation as a risk theme. Globally, CPI inflation reached almost 9% in 2022 due to the Russian invasion of Ukraine and is projected to peak at over 4.5% in 2026 as a result of the US/Israel-Iran war. In both cases, the cost pressures associated with energy price spikes reduced real disposable incomes, weakening demand and causing downwards revisions to the baseline forecast for GDP growth.

In contrast, our downside IFRS 9 and CECL scenarios see inflation fall below baseline levels, rather than rising further. This is due to our statistical methodology for scenario construction. We use forward-looking probability distributions for key metrics such as GDP, unemployment, and house prices to define the severity of the scenarios. This statistical approach addresses the unbiasedness requirement under the IFRS 9 standard. It also enables us to attach well-defined probability weights to each scenario. Finally, our methodology also succeeds in keeping scenarios relatively stable across quarters, thus limiting excess volatility in our clients’ provisioning against future credit losses.

This approach differs from a narrative-based approach to scenario construction, in which assumptions are applied in a “bottom-up” fashion. A narrative-based approach allows new emerging risk themes to be modelled explicitly, thus enabling lenders to capture the specific risks auditors and internal stakeholders are worried about at that point in time. However, this comes at the cost of introducing more subjectivity to scenario construction and probability weights. Not all portfolios are equally impacted by the US/Israel-Iran war, for example. In addition, a narrative-based approach to IFRS 9 and CECL scenario modelling necessarily leads to increased volatility in scenarios and thus in P&L, as risk themes change over time. Finally, a narrative-based methodology tends to capture only current or expected downside risks but would normally struggle to also capture unspecified future downside risks as the source of these will remain uncertain until they materialise. Reflecting the multiple shortcomings from this approach, we do not recommend the use of narrative-based scenarios for ECL calculation under IFRS 9 or CECL.

The treatment of inflation in alternative scenarios is a key demonstration of the differences in modelling approach. Under our statistical approach, a downside scenario sees a moderation in demand and GDP and rising unemployment. Reduced aggregate demand, in turn, leads to weaker inflationary pressure when compared to the base case. There is no compensating shock to commodities prices, population growth or other supply disruptions which could offset the deflationary impact from increased demand-side weakness, given the subjective nature of taking such assumptions. Narrative-based scenarios on the other hand may boost inflation above baseline rates by overlaying additional shocks to any number of supply side factors. This allows narrative-based scenarios to explore downside risks from increased inflation when that risk is topical.

Whilst inflation and higher policy rates have been prominent downside risk themes since the end of the Covid-19 pandemic, even over this short time window this has not consistently been the case. Before the renewed inflationary pressure from the US/Israel-Iran war, focus had returned to how quickly rates and inflation would normalise. Furthermore, prior to the pandemic, there was much discussion in the economics profession about how to raise inflation, which was seen as being depressed by various structural factors including demographics and excess supply from China in some industries. As war risk and disruption to oil markets are resolved, narrative-based downside risks will again shift to other topical events. Instead of moving with these narratives, our distribution-driven approach ensures that we focus on the structural dynamics between inflation and demand which have not changed during various supply-side shocks in recent years.

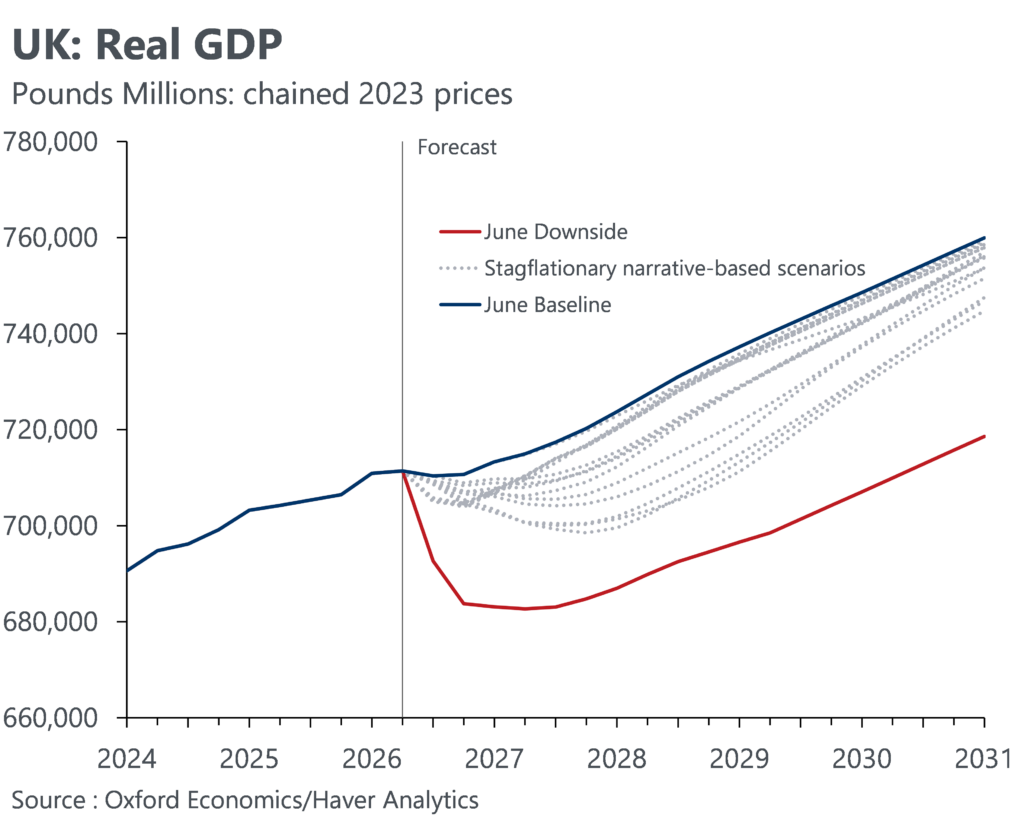

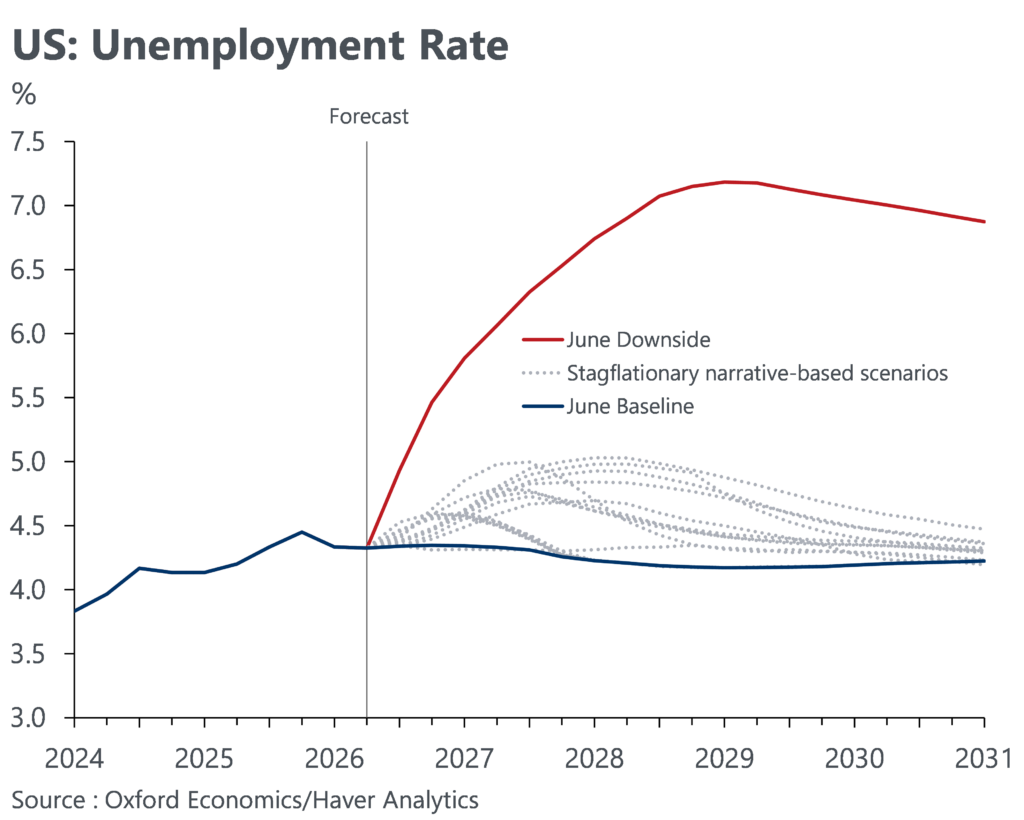

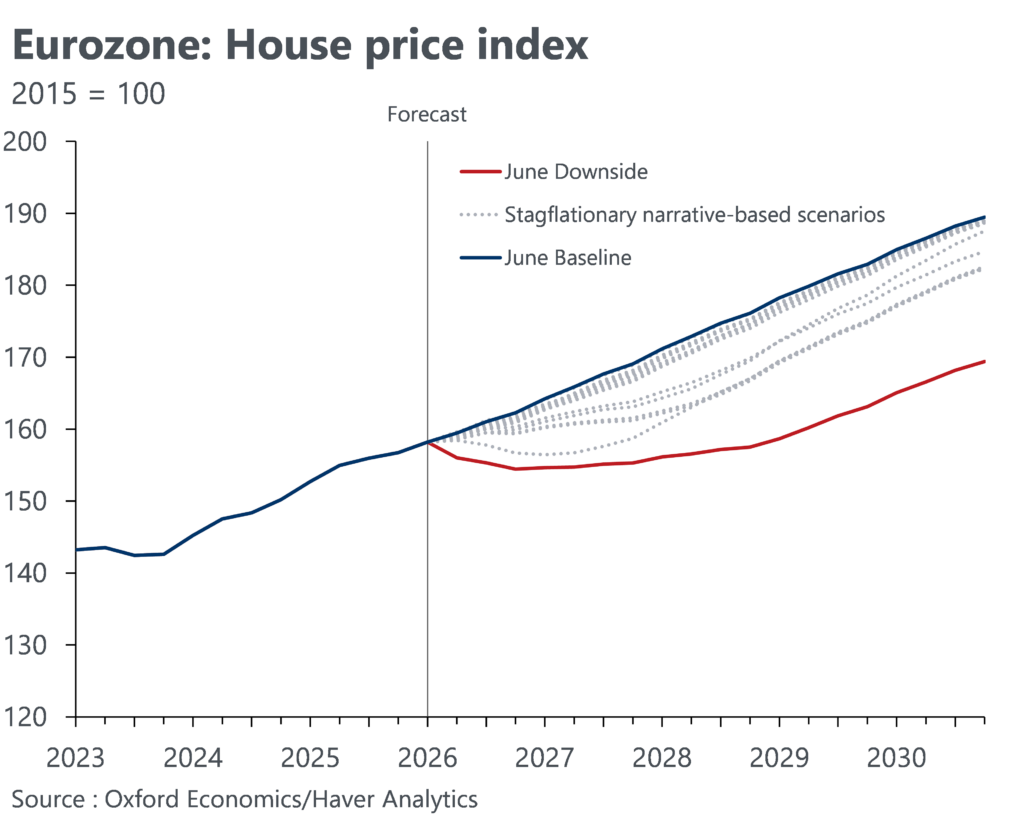

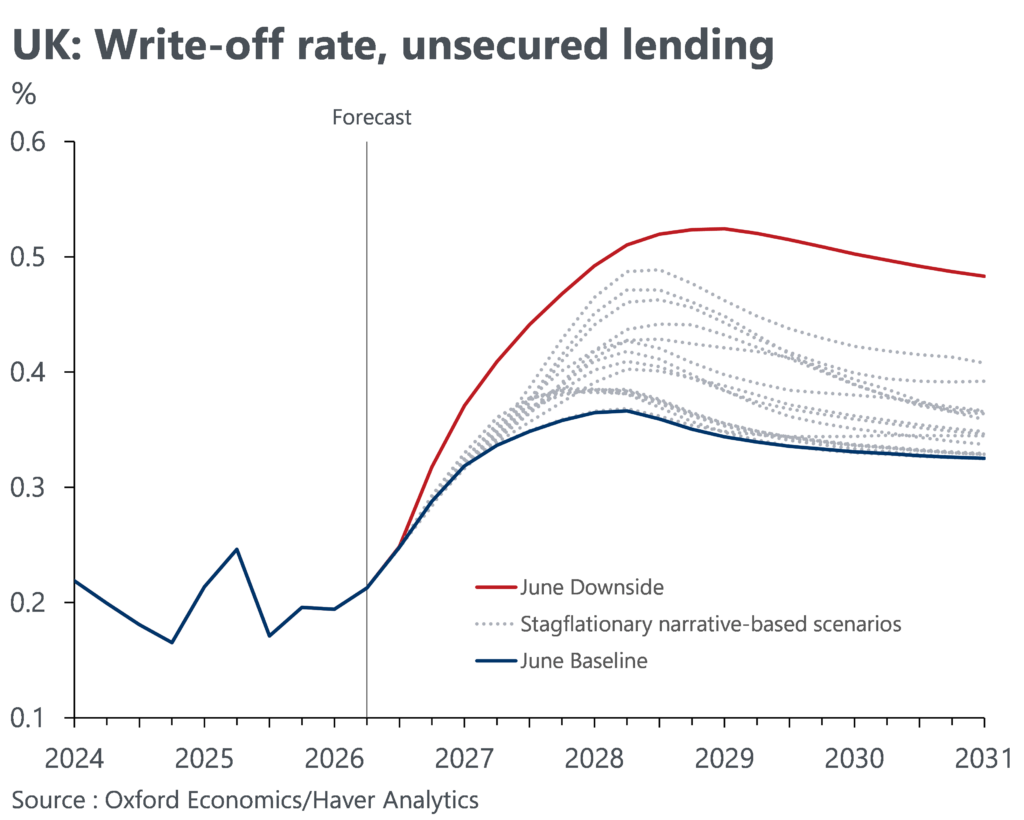

As part of our wider scenario analysis for clients, Oxford Economics also constructs narrative-based scenarios which have included stagflationary shocks over the past few years. We routinely compare the impacts in our IFRS 9 and CECL downside scenarios against these narrative-based scenarios to ensure that our IFRS 9 and CECL scenarios capture current risks well. We find that our downside scenarios are generally more severe for key drivers of impairment such as unemployment rates, house prices, and GDP. As shown in the accompanying charts, our downside IFRS 9 and CECL scenario, modelled at the 85th percentile of our forward-looking distribution, is persistently more severe than the stagflationary scenarios modelled in our Global Scenarios Service since 2022. Hence, although our downside IFRS 9 and CECL scenarios do not explicitly model stagflationary risk themes, the representativeness and severity of our statistical scenarios ensures that they implicitly capture the spillover effects on key drivers of credit losses from stagflationary shocks.

An exception in this context is the impact on interest rates and inflation itself. In our downside scenarios weakened inflation leads to lower policy rates as central banks shift their policy stances to support economic activity. The opposite holds true in upside scenarios. While this may lead to counterintuitive results in some credit loss models, it is important to keep in mind that policy rates tend to act as a proxy for credit conditions more generally. Using more direct measures of credit and borrower stress, such as write-off rates, insolvencies, and debt burdens, overcomes this challenge and ensures a more precise model since the combined effect from the wide range of factors impacting these measures is captured. Indeed, in our downside IFRS 9 and CECL scenarios write-off rates, insolvencies and debt burdens all rise as the positive impact from lower interest rates is more than offset by the sharp deterioration in labour markets, incomes and asset prices.

Clients wishing to analyse the impact from stagflationary scenarios on their portfolios can explore our Global Scenarios Service which examines topical risks that are updated each quarter. We also model narrative-based scenarios on a bespoke basis for clients, such as for the purposes of risk analysis, ICAAP stress scenarios and regulatory stress scenarios.

Click here if you want to learn more about our IFRS 9 service and here for our CECL service.