Higher tariffs to reduce construction rebound

We have produced an interim Global Construction Forecast update to reflect the fast-changing trade environment. We have lowered our growth forecasts by 1.3ppts in 2025 and 0.9ppts in 2026. This downgrade is less than we anticipated following the ‘Liberation Day’ announcement as the US administration has delayed the reciprocal tariff element of the announcement.

The primary impact of the tariffs on construction is through reduced private sector investment. Increased uncertainty amplifies the risks around investment decisions, thereby reducing financing of construction work. The US and Asia face the biggest downgrades, with the Industrial building sector being the most exposed.

Our forecasts assume US tariffs on the rest of the world remain at 10%, with three exceptions. We assume the average effective tariffs on Canada and Mexico will be 13% and 15% respectively but will fall below 2% when a new USMCA trade deal is negotiated next year. We assume China’s average tariff will remain above 100%.

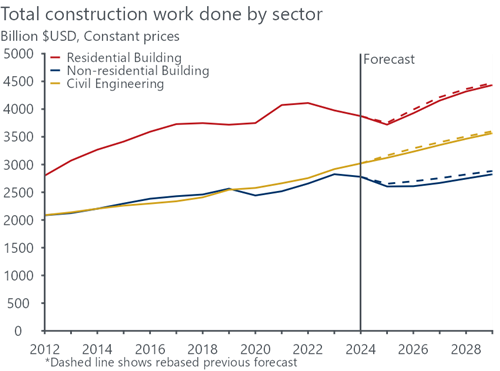

Chart 1: Increased uncertainty from ‘Liberation Day’ will weigh on construction activity