Australia Faces Election risk, but migration stabilisation on track

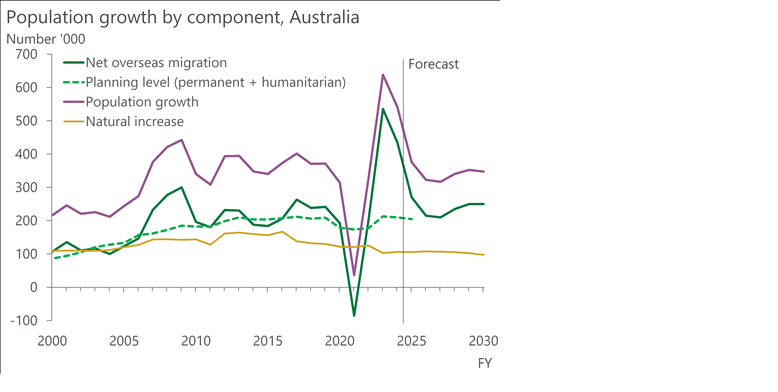

The cumulative outlook for net overseas migration (NOM) is largely unchanged from six months ago, but timing has been tweaked. 2025 is modestly stronger, countered by the medium term being revised down.

Factoring in the September quarter demographic data, we expect a quicker tapering in NOM than assumed in the 2025-26 Federal Budget. It is forecast NOM will slow to 270,000 in FY2025 before sliding further to a trough of 210,000 persons in FY2027. It is not until FY2029 that we forecast a return to a steady state level of 250,000 per annum.

The current slowdown is evident across most key visa streams, but international students dominate and are where the largest fallback resides – grant approvals were down 32% y/y over the first two months of 2025. We stress that this is a normalisation from a record base. While there are challenges, the international student market remains fundamentally sound.

A suite of policies impacting students were actioned in 2024, including higher fees and testing standards. The proposed student cap failed to pass parliament, but Ministerial Direction 111 was introduced as a workaround in December. This created visa prioritisation streams based on provider level caps which aggregate to 270,000 new commencements a year.

Our revised NOM outlook allows for an increased volume of departures. There is a growing stock of temporary visas with expiry dates nearing and stay rights have been dialled back in areas. We still assume a fair degree of stickiness across ‘long-term’ temporary migrants in Australia. There is material downside risk if the visa rollover environment proves more restrictive.

Recent tariff instability does little to impact the outlook for migration, with the lower dollar likely enough to offset any uncertainty for those considering a move. The outcome of the upcoming election in May is more substantive, with a change in government representing downside risk.

The normalisation of NOM set to continue through 2025