Will the European Union’s recovery mark a shift towards a green economy?

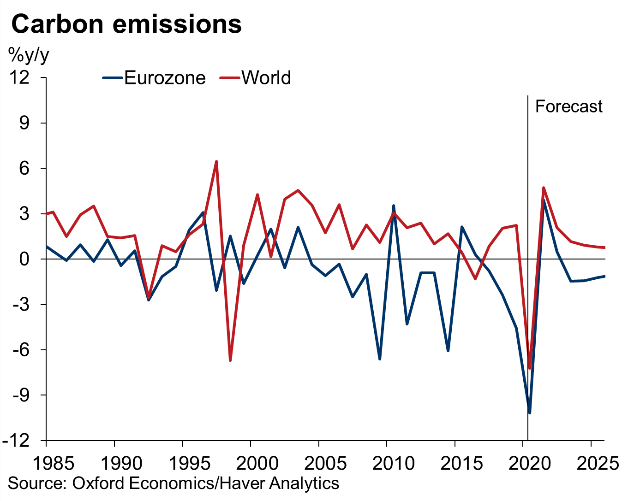

In his recent blog post, Ahmed Esam discusses the challenges the GCC region faces as it aims to transition away from its reliance on oil production. Not being a big oil producer, Europe doesn’t face the same obstacles as the GCC. But greening the EU’s carbon-intensive energy sector and heavy manufacturing industries will nonetheless require enormous effort. Indeed, the COVID-19 pandemic saw carbon emissions drop in 2020, but the economic rebound this year will see emissions soar, especially in countries that are more reliant on oil.

The European Union is committed to following its decarbonisation policy and carbon-neutral target. Fiscal and monetary policy plans will aid the EU’s (recently upgraded) pledge to reduce its carbon emissions by 55% (compared with 1990 levels) vs. the previous goal of 40% by 2030 to reach climate neutrality by 2050. The announced and expected fiscal and monetary policy plans at the EU level are unlikely to be enough to attain the goals on their own, but together with national and EU plans and commitments, such as CO2 price and other regulatory requirements, they should support the greening of the economy.

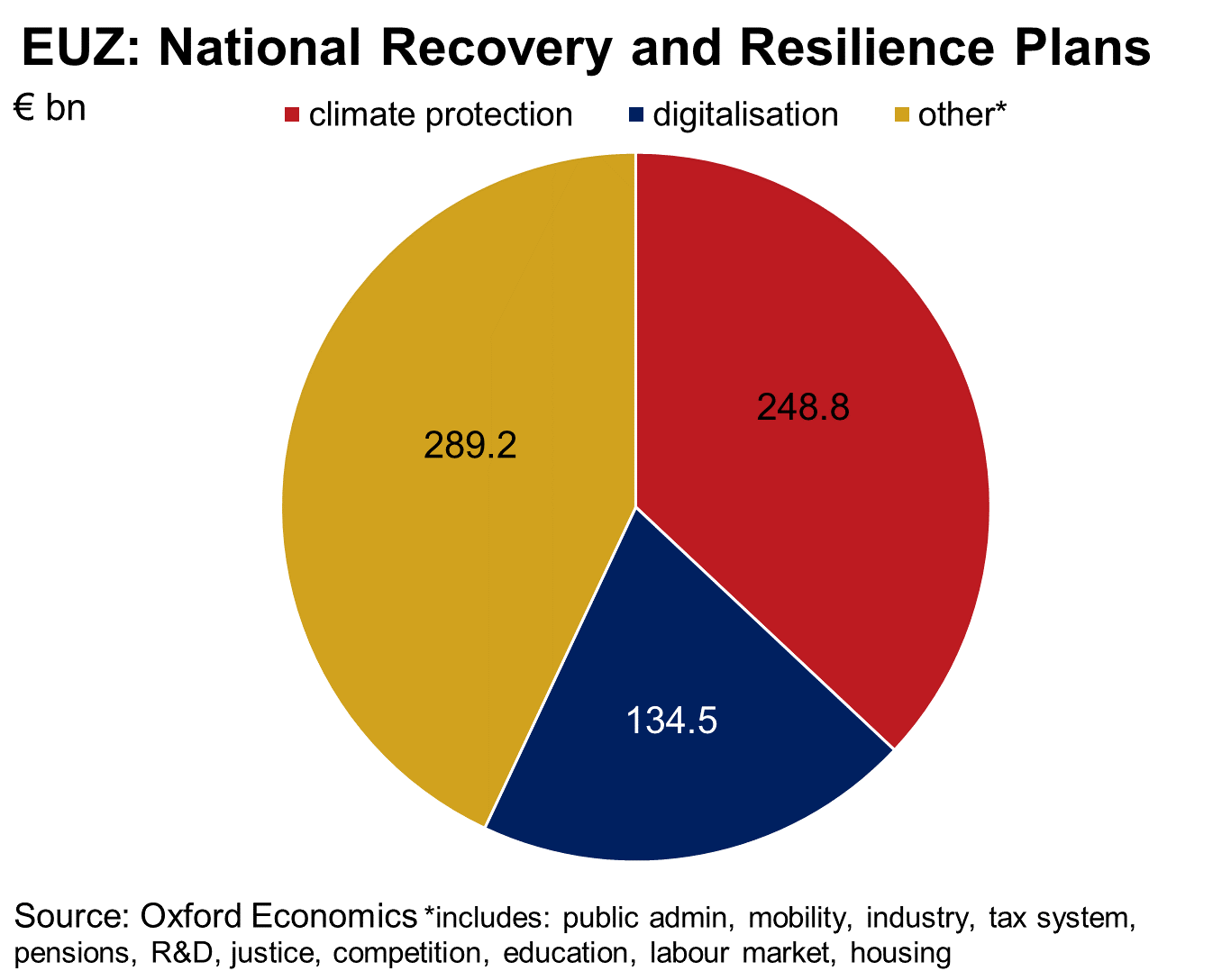

In terms of fiscal tools, the Recovery and Resilience Facility (RRF) is adding to existing plans by providing roughly €672.5 bn in finance support for the bloc’s recovery. The RRF requires countries to spend at least 37% on climate protection. While this is an important step towards a more sustainable climate policy, we caution that the impact of this spending (equal to 1.9% of the European Union’s 2019 GDP) is not nearly large enough given the challenge. To put this into perspective, the DIW Berlin (the German Institute for Economic Research) estimates that investments worth €3 trillion are required to achieve climate neutrality by 2050.

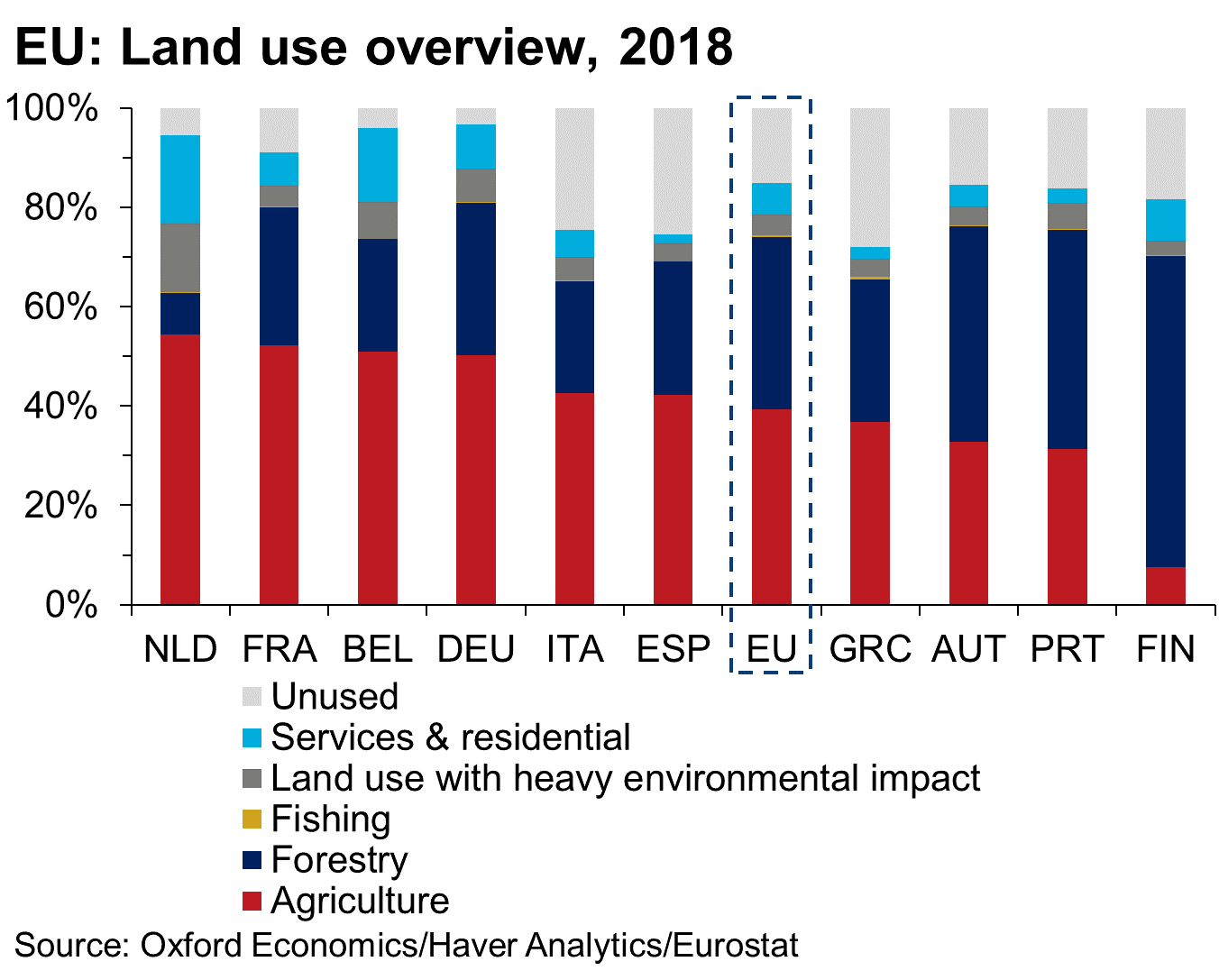

Although government plans are well intended to steer the transition to a greener economy, their effect is often limited. One example is transportation—tax incentives to purchase electric vehicles are a step in the right direction, but as long as the electricity used to charge the vehicles is not green, the effect is merely a redistribution of emissions from city centres to power plants. And despite these incentives, the share of electric vehicles remains small. Another example is the agricultural sector, which is lacking progress in climate change mitigation with below-average emission reductions. Since around 39% of the EU’s land is used for agriculture and 35% of the EU budget is spent on that sector, this could be a large policy lever. Within the EU’s Common Agricultural Policy (CAP), the EU is incentivising sustainable agriculture and biodiversity. But steering EU farm subsidies away from livestock and consumer demand away from emission-intensive products such as dairy and beef has been difficult, and emissions from the agricultural sector remain high.

The second tool, monetary policy, should support the eurozone’s transition towards a greener economic system but will be insufficient to enforce change. European Central Bank (ECB) president Christine Lagarde’s push for the ECB to support the EU’s climate plans and the bank’s ongoing strategy review set the stage for the ECB’s support for a greener economy subordinate to its primary goal of maintaining price stability. There are four main channels in which the ECB can promote green investment. First, the ECB can support the shift towards a carbon-neutral economy via its own investment portfolio. However, the portfolio itself is too small to have a macroeconomic impact. Second, the ECB could move towards a “greener quantitative easing,” and focus its corporate sector purchase programme (CSPP) more on the services sector, which tends to have lower emission shares compared with industry. However, this approach only works as long as below-target inflation requires the central bank to purchase assets to support the recovery. Our forecast sees the eurozone approach its inflation target by 2027, long before climate goals can be achieved. Third, a permanent mechanism could be to generate incentives via the interest rate channel for corporate financing to invest in green projects. Depending on the climate rating, climate footprint or ESG score, different rates may be offered for corporate bonds, which serve as collateral. The ECB hasn’t taken action in this direction yet, but it could become a long-term objective. Fourth, the ECB is planning to require banks to assemble information on their climate risks of stranded assets. This information could help drive adjustments in banks’ strategies as this information is disclosed, and steer the transition to a climate-neutral financial system in the future, but will have no impact in the near-term since no action has been taken yet.

The fiscal and monetary stimulus provided to support the European Union’s recovery from the pandemic will be too small to lead to sustainable structural changes and a green economy. We expect carbon emissions to snap back as economic activity resumes, buoyed by pent-up demand. To address climate imperatives, executives should focus on green investments, minimise financial risks from climate change and work towards a smooth transition to a carbon-neutral economy.

Tags: