Research Briefing

| Jul 23, 2024

The future of industrial activity in Europe

Our forecasts do not show any significant deindustrialisation over the next decades in Europe—in fact, we find predictions around imminent or longer-term deindustrialisation to be overblown. The term, initially coined to help spur a political response to the energy crisis of 2022, has morphed into a catch-all that tends to confuse the structural and cyclical headwinds Europe has been facing.

What you will learn:

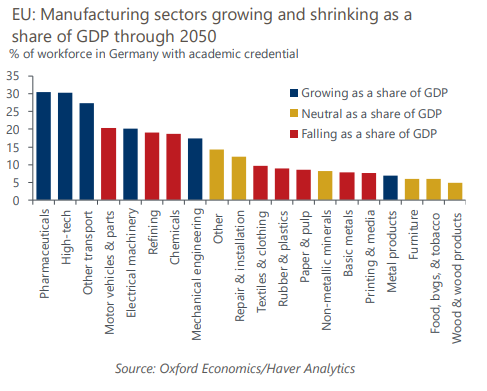

- The continent faces significant challenges that will weigh heavily on low skilled, upstream, energy intensive, and easily tradeable sectors. We think these sectors will shrink as a proportion of GDP and, in some cases, on an absolute basis. Textiles and basic metals have already experienced decades-long decline as energy and wage costs have increasingly made production within Europe uncompetitive. In other cases—most prominently chemicals—the energy crisis acted as a negative shock that will leave output permanently lower and less important for future overall economic activity.

- The reason we do not think this will translate into deindustrialisation is that the decline of some industries will be offset by the rise of others. Europe retains significant advantages in specialised and high-knowledge, high-skill sectors. Mechanical engineering, electronics, pharmaceuticals, and electrical machinery are examples of such sectors that we expect will rise as a proportion of economic activity, offsetting declines in other industries.

- The shift towards such industries, as well as structural challenges in the automotive sector related to demographics, foreign competition, and the transition to EVs, means that while industrial output growth is likely to remain robust, it is unlikely to be as large of a source of job creation as in the past. This can help explain political anxiety around deindustrialisation as, from the perspective of workers, the future does indeed not look as bright as it once did.