Prolonged war in Iran could tip the global economy into recession

By Ben May, Bridget Payne and Paul Moroz

The conflict in the Middle East is already rattling global energy markets. Our baseline economic forecasts assume a sustained period of disruption to both energy production in the Middle East and shipping traffic through the Strait of Hormuz. But what if things get significantly worse? We’ve modelled a “Prolonged Iran War” scenario using our Global Economic Model — and the results are sobering.

A perfect storm for oil supply

We assess the implications of a stalemate between the US/Israel and Iran which leads the Strait of Hormuz to stay effectively closed for six months — exacerbated by Iranian strikes on alternative pipeline routes through Saudi Arabia and the UAE, and a resurgence of Houthi attacks in the Red Sea.

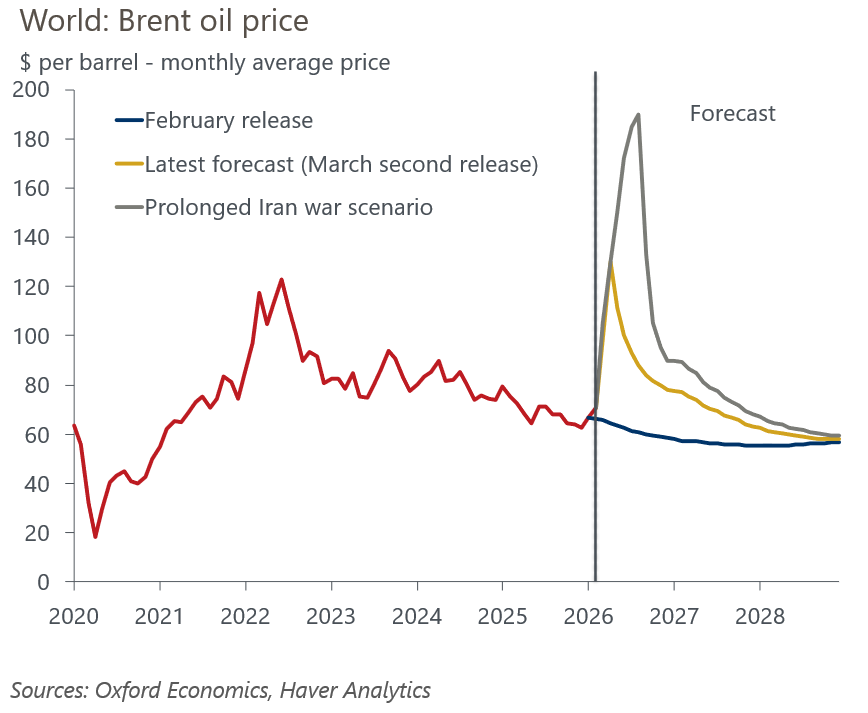

Global oil supplies drop by nearly 20 million barrels per day. Commercial inventories halve by mid-year, reaching critically low levels within the following three months. Brent crude surges to around $190 per barrel in August, surpassing the 2008 all-time high of $147. Refined products — diesel, jet fuel, and shipping fuel — spike harder still. European and Asian natural gas prices rise to $30/MMBtu in Q3, pushing up electricity prices and complicating winter storage replenishment.

Losing almost 20% of global oil supply leads to shortages, rationing, with effects that go far beyond demand destruction from higher prices. Around two-thirds of global oil consumption is transport-related, and diesel is the backbone of commercial logistics, agriculture, and parts of industry, so disruption would hit the economy through multiple channels. Physical rationing in H2 2026 would constrain activity directly, compounding the impact of higher prices.

A rare global recession

Global inflation hits 7.7%, close to the 2022 peak. But unlike 2022, when the global economy kept growing through the price shock, the severity of this disruption tips the world into outright contraction.

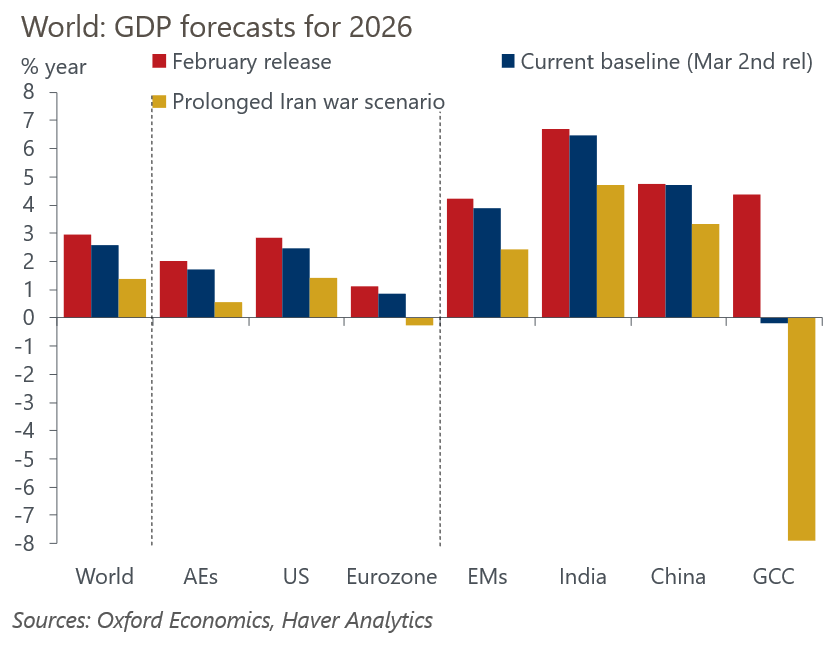

World GDP falls in the middle of the year and the calendar year growth rate for 2026 slows to 1.4%, 1.2 percentage points below our baseline, before a modest recovery to 2.1% in 2027. The US and most major advanced economies slide into recession; China’s growth falls to 3.4%. The last times the global economy contracted were during the pandemic and the global financial crisis. This would be the worst synchronised downturn in 40 years outside those two events.

Who gets hit hardest?

The Gulf states suffer most acutely — GDP down over 8% in 2026 — before rebounding sharply as production recovers. Advanced Asian economies, which are especially reliant on Gulf oil take a heavy blow from energy import cost surges and supply chain disruption. Europe faces a painful squeeze on gas and electricity. The US fares somewhat better given its domestic energy production, but an equity market decline of nearly 20% weighs heavily on consumer spending.

Central banks in a bind

The ECB and Bank of England are expected to raise rates by 100bps this year, prioritising inflation credibility over growth. The Fed, by contrast, is modelled cutting rates — leaning into the labour market side of its dual mandate as unemployment rises. That policy divergence has ambiguous implications for the dollar: rate differentials point to weakness, but safe-haven demand in a risk-off environment could offset that, at least initially.

What if it gets even worse?

The scenario is already severe, but the shock could prove more damaging still. Physical fuel shortages may be larger and stickier than modelled, with knock-on effects for core inflation and a harder trade-off for the Fed. A pullback in US AI infrastructure investment — triggered by semiconductor supply constraints or tighter financial conditions — could deepen the downturn materially. Most consequentially, two significant inflation overshoots within four years risk de-anchoring expectations, embedding higher inflation risk premia into long-term rates and making the economy structurally more sensitive to future supply shocks.

The world is not yet in this scenario. But the mechanisms that would take us there are very much in play.

In our latest webinar, our economists demonstrate how to quantify the economic impact of the Iran conflict under alternative scenarios.

Using our Global Economic Model, we show how energy shocks feed through trade, inflation, and global growth—providing a structured framework for navigating uncertainty.

You might also be interested in

Subscribe to our newsletters

Sign up to our newsletter to download the latest and most popular reports.

Subscribe