Research Briefing

| Sep 9, 2024

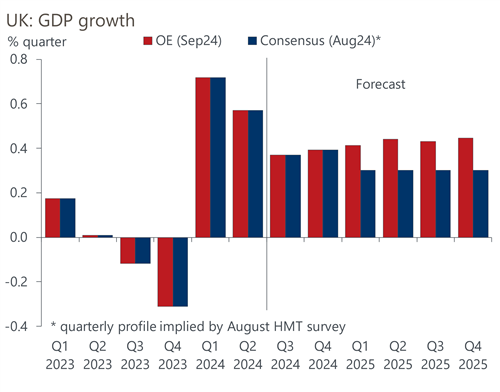

Growth may slow, but the consensus looks too weak

The UK grew at an above-trend pace in H1 2024, but we don’t expect this to be sustained over the next couple of years. However, we are more optimistic than the consensus. Our forecast that GDP will grow by 1.7% next year is based on the notion that consumers will finally shed their caution and make a stronger contribution to growth.

What you will learn:

- The likelihood that fiscal policy will be tightened in the Budget on October 30 is a key reason why we expect growth to slow. Our forecast assumes the Chancellor will implement an extra £10bn (0.4% of GDP) worth of tax increases from next year, on top of the measures set out in Labour’s election manifesto.

- But a larger tightening is possible, particularly if the Chancellor decides not to tweak the fiscal rules to remove the impact of Asset Purchase Facility losses

- We’re now in the early stages of an interest rate cutting cycle, with the Bank of England’s messaging consistent with 25bps rate cuts at every other meeting. While companies should benefit from rate cuts fairly quickly, for the household sector the lagged impact of past rate hikes will continue to dominate over the next eighteen months.