Downside risks for Asian industrial real estate markets

Reduced business investment, weaker confidence, and risk-off sentiment alone will inflict a demand shock on industrial and logistics operators, with expansion plans likely on hold.

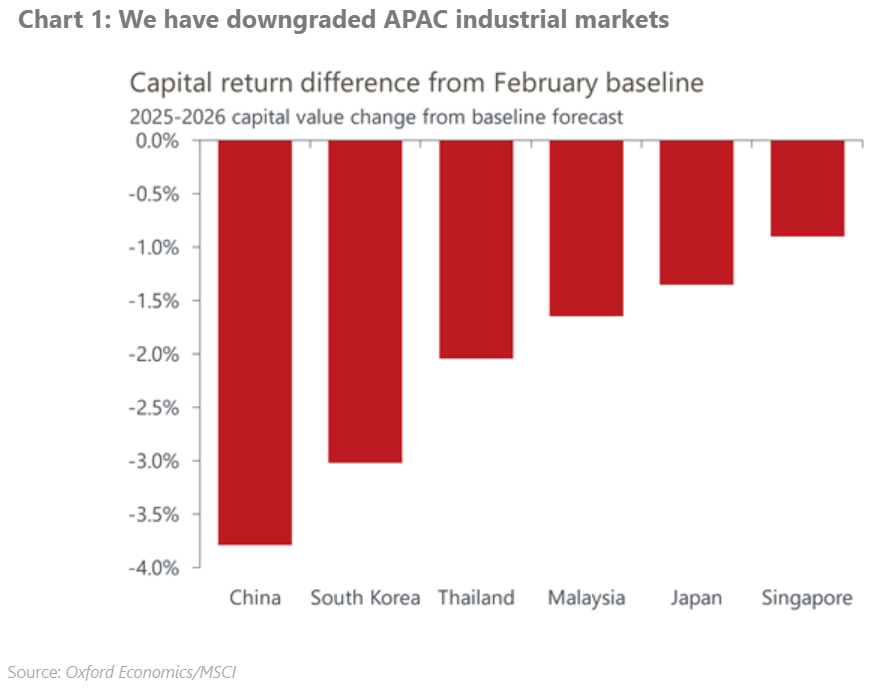

The ‘liberation day’ tariffs have been postponed, but the existing tariffs and those likely forthcoming present significant downside risks for most Asian industrial real estate markets. Reduced business investment, weaker confidence, and risk-off sentiment alone will inflict a demand shock on industrial and logistics operators, with expansion plans likely on hold.

Auto tariffs also remain at 25%, which will heavily impact South Korea and to a lesser extent Japan. ASEAN markets are also likely to face higher future tariffs, but supply chain shifts in those markets will remain sticky.

China of course faces a more severe downside, given the current tariff levels. With overcapacity evident in industrial production, alongside significant oversupply already in industrial real estate markets, operating fundamentals in the industrial real estate sector are likely to deteriorate as occupier demand stagnates.

While benchmark rates are likely to decline, risk premia are rising. We anticipate little-to-no benefit from falling benchmark rates as investors looking at tariff-exposed sectors, such as industrial real estate, will remain cautious and demand higher returns.