Why the UK should invest in the industries of the future

The UK needs a strategic vision if it wants to arrest the stagnation that has plagued the economy — and targeted industrial policy may be a good place to start. There has been a shift in the global narrative around industrial policy and whether this derives from de-risking supply chains, helping the green transition, or getting a head start on sectors with large growth prospects.

It is imperative the UK identifies and engages in shaping these industries of the future. Our analysis of the 2024 Spring Budget and last year’s autumn statement, as well as the current state of the market in battery production, data centres, and life sciences, suggests more needs to be done.

Headwinds to growth

The Department for Business and Trade’s 2023 UK battery strategy committed £2 billion of new capital and R&D funding for zero emissions vehicles, batteries, and their supply chains between 2025 and 2030. This may sound like a large investment, but this figure refers to investment across the entire value chain rather than simply the construction of gigafactories for battery manufacturing. The current pipeline sees a capacity shortfall of 33% in EV battery requirements for 2030. Bearing in mind that a single gigafactory can cost multiple billions of pounds, the scale of investment needed becomes apparent.

Data centres have been an area of strength for the UK economy as London’s position as a global financial hub gives the sector a head start by providing a strong base of energy infrastructure. Google’s recent $1 billion investment in a new data centre in Hertfordshire shows that the UK is still an attractive market.

However, two main headwinds threaten to halt the growth. A skills shortage created by a weak pipeline for trained contractors is leading to increasing wage competition, pushing companies to look for new markets. Energy demand is rising faster than we are building new supply, placing pressure on energy grids. A focus on upskilling labour and improving the energy infrastructure across the UK can ensure that investment in the sector can flow into the UK.

Life sciences is one sector the government itself identifies as a “growth priority” and last year’s autumn statement provided £520 million of new funding to manufacturing in the sector. The UK industry has fostered significant advancements, such as the first Covid-19 vaccine, partly by leveraging the strength of the university sector. There have been calls for more spending in this area with some pointing out the global cost-benefit analysis for vaccine developments can be in the region of 20:1, the equivalent of spending £1 million and receiving £20 million worth of benefit. The UK has an opportunity to be a global leader in this sector but currently it only employs a relatively small proportion of the UK population, so directing more investment into it would require clear strategic foresight and planning for growth.

Fig. 1. Total GVA contribution to UK GDP by the manufacturing sector, 2022

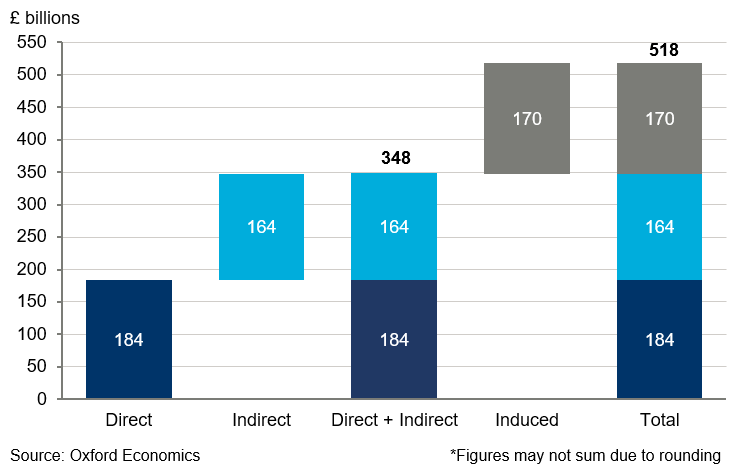

The pattern across these sectors is that currently there is a strong base that can be built upon to turn them into high growth areas. Our research into the manufacturing sector in the UK points to the wider benefits of investment in manufacturing beyond companies within the sector. While manufacturing firms contributed £184 billion to the UK economy in 2022, once their supply chains and employees’ spending are included that rises to half a trillion pounds (Fig 1).

Whether through more long-term policy planning, attracting investment, or increased infrastructure spending there are good opportunities for growth within manufacturing and industrial policy. The government should take note of the change of wind in industrial policy and direct investment to critical infrastructure to ensure the UK doesn’t muddle its way through to a period of stagnation.

Author

Tags: