Research Briefing

| Oct 17, 2022

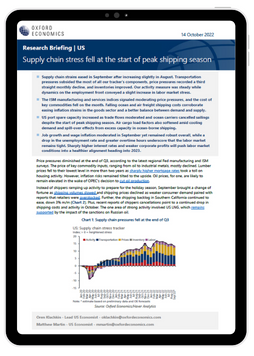

US supply chain stress fell at the start of peak shipping season

Supply chain strains eased in September after increasing slightly in August. Transportation pressures subsided the most of all our tracker’s components, price pressures recorded a third straight monthly decline, and inventories improved. Our activity measure was steady while dynamics on the employment front conveyed a slight increase in labor market stress.

What you will learn:

- The ISM manufacturing and services indices signaled moderating price pressures, and the cost of key commodities fell on the month. Falling ocean and air freight shipping costs corroborate easing inflation strains in the goods sector and a better balance between demand and supply.

- US port spare capacity increased as trade flows moderated and ocean carriers cancelled sailings despite the start of peak shipping season. Air cargo load factors also softened amid cooling demand and spill-over effects from excess capacity in ocean-borne shipping.

- Job growth and wage inflation moderated in September yet remained robust overall, while a drop in the unemployment rate and greater overtime hours underscore that the labor market remains tight. Sharply higher interest rates and weaker corporate profits will push labor market conditions into a healthier alignment heading into 2023.