The ‘new Great Stability’ conundrum for the world economy

It is plausible that recent low volatility is the new and persistent norm, with economic surprises muted and downside risks in decline.

As a tempestuous year in world politics comes to an unnerving close, in economics the nervousness flows from an almost entirely and strangely opposite cause. 2017 ends as the year of the risk conundrum.

Even as the advent of the Trump Administration, the UK’s great Brexit gamble, and the rise of populism and separatist tendencies in parts of Europe have raised the global political stakes, in the global economy both macro and market volatility have recently plummeted. Conditions, in fact, appear more stable than during the period of the Nineties and early 2000s, which itself became known as the ‘Great Stability.

And it’s not just realised volatility that has fallen; more subjective measures of global risk have also declined significantly in recent years.

For some this will sound too good to be true. How can risk have plummeted so soon after the global financial crisis, the riskiest period for decades? Growth is weak, inequality has grown, asset prices appear inflated relative to fundamentals and at risk of sharp adjustment.

Indeed, proclamations of stability represent major hostages to fortune. The International Monetary Fund’s April 2006 Global Financial Stability Report trumpeted stability at exactly the wrong time and for the wrong reasons, spectacularly mis-stating even the report’s title. And much excellent academic work was conducted on the Great Stability, which in the UK culminated in an international conference – whose opening was delayed by the announcement that the Bank of England had bailed out Northern Rock. We are warned!

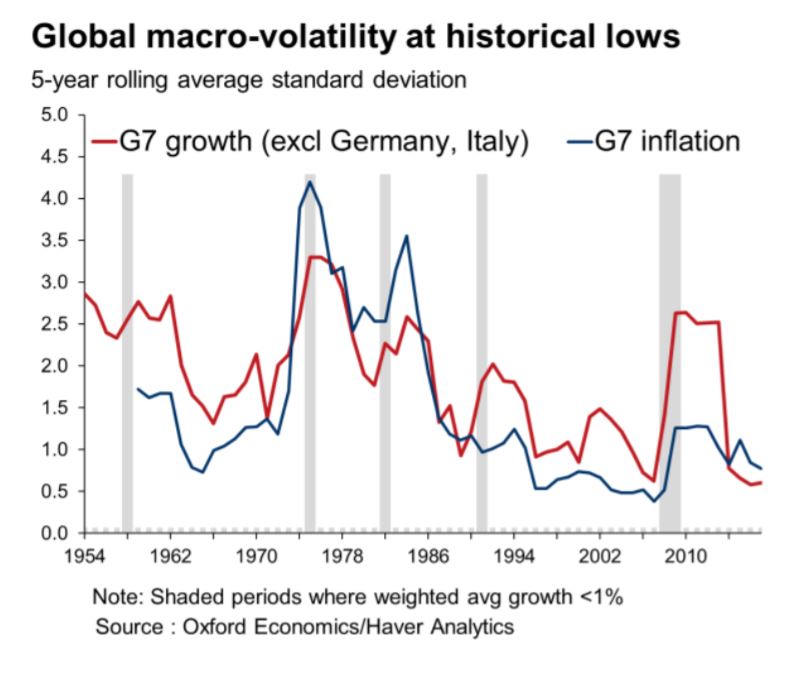

And yet, there is growing evidence that the global economy may indeed have entered a sustained period of stability. Reduced macro-economic volatility is apparent across an array of measures.

Macro and financial volatility have fallen

In the historical major economies, the standard deviation of GDP growth and inflation – how far these vary from longer-run averages – has fallen dramatically. Across countries, dispersion of real experience for key macro-variables is also at record lows – implying that there are fewer advanced economies growing or shrinking at worrying rates.

In markets, it’s not just the well-known VIX index of near-term US equity market volatility that has plunged. Realised volatility has also fallen. The size of daily changes in the S&P500 index of US blue-chip stocks over the past year has been at around the lowest in half a century. In bond markets, as well, options have priced in record-low volatility.

Economic surprises more muted and fears over risks have faded

The accuracy of professional forecasters has improved accordingly. In the decade prior to the great financial crisis, there was typically a sizeable gap between the mean consensus forecast for global growth and the actual outturn; in the years following the crisis, the absolute forecast error has, on average, been less than a quarter of the size

Our own Oxford Economics Global Risk Survey meanwhile provides evidence that concerns over key near-term macro and market risks among leading businesses worldwide have diminished over the past couple of years, both on the downside and the upside.

The OE survey results are also in line with our scenario analysis. Each quarter, the Global Scenarios Service quantifies the potential impact of key risks. Our scenarios this year have suggested much more moderate implications for the global economy than the key risks earlier in the decade.

Risks to the global economy more balanced

Consistent with reduced concerns over high-impact risks such as a China hard landing, the risks to global growth prospects currently appear more balanced than for some time. That is also reflected in our global scenarios.

Weighting together the world GDP growth profiles across these scenarios, we can estimate a mean profile for global growth. The gap between this mean profile and our baseline forecast has fallen markedly over the past couple of years, in line with the idea that risks to global growth are no longer heavily skewed to the downside.

Other forecasters more certain

Against this backdrop, key international institutions have, like respondents to our Global Risk Survey, become increasingly confident over the near-term path for global growth.

Every six months, the IMF publishes its estimates of the confidence intervals around its central forecast for global growth. These intervals have shrunk considerably since the start of the decade. Meanwhile, in the US, the dispersion of views on the US Federal Reserve’s policy-making Open Market Committee (FOMC) on the most likely path for US growth has fallen steadily – and now stands at a level last seen prior to the financial crisis.

The root causes for all of this are similar to explanations for the so-called Great Stability (late 1980s-2006). These include structural changes involving more flexible product and labour markets; better policy-making leading to an anchoring inflation expectations; and luck (emerging market strength as a counter-weight to advanced economy stress in recent years, after the Great Stability experience of smaller, less persistent shocks than in the 1970s/80s).

More ‘grating’ than great

The current period of stability does appear more “grating” than “great”. Low macro-volatility has been associated with weak trend growth, income inequality and elevated political risks. There are also worrying financial market valuations, and concerns over financial risk-taking and capital structure rejigging that have underpinned the rise in corporate debt in the US and EM.

But we are comforted that balance sheet risks appear less extreme than in 2006. Growth in assets of leveraged institutions has been modest since 2009, and pockets of credit risk in parts of the economy appear much less systemic than then.

Against this backdrop, it is plausible that recent low volatility is the new and persistent norm – in line with the Great Stability and in contrast with the great financial crisis.

{{cta(‘e938f0ae-fe14-4a8e-9187-3b6bc5d3a42b’)}}

Tags: