Silver lining for China’s residential real estate sector

Residential real estate will make a slow recovery over the near term.

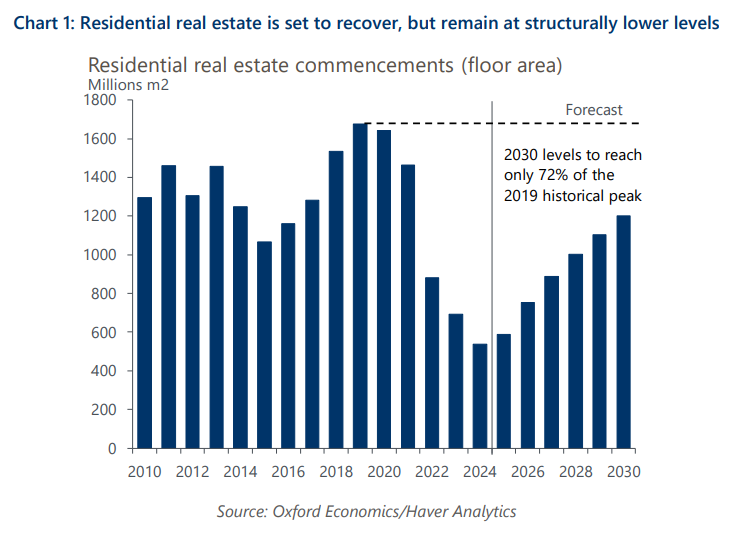

Residential real estate commencements (floor area) are expected to pick up over 2025. However, activity will remain at structurally lower levels, with Chinese authorities expected to maintain their goal to clamp down on speculative demand.

China’s residential real estate sector shows signs of stabilising, with prices for existing housing in tier 1 cities continuing to improve through to March 2025. Despite Vanke’s fallout, which was ultimately the consequence of the state induced property correction, confidence in the property sector is expected to recover slowly.

Stimulus measures announced over September and October 2024, have helped the completion of unfinished projects and destock inventories. Fiscal support for state-owned enterprises to purchase existing housing inventory and convert it into affordable housing as well as the renovation of urban villages, old residential quarters and shanty towns will also remain supportive over the medium to longer term. We expect policy aimed at housing affordability will be more in-line with the Singaporean model.

As part of a renewed urbanization effort, the State Council announced a five-year action plan which aims to raise the number of urban residents from a current 67% to 70% in 5 years. We anticipate governments efforts to continue in the same vein further into the long term.