Research Briefing

| Mar 10, 2025

Next German coalition launches fiscal bazooka at new geopolitical realities

New geopolitical realities have forced the likely next German coalition of the CDU and SPD into agreeing to a massive fiscal splurge. Details are scarce and implementation risks loom large, but this could in theory see the fiscal deficit widen to 4% of GDP for the next decade. The measures could help build a viable military deterrent, jumpstart the recovery and transform the economic outlook for the coming decade.

What you will learn:

- The scale and urgency of the proposal suggest that this is in part a political signal to allies and adversaries. However, the required support from other parties isn’t yet secured, and a coalition deal could yet fail to materialize. The proposal also targets a long-term reform of the debt brake, which may envisage less ambitious easing. And the economy may struggle to absorb all funds.

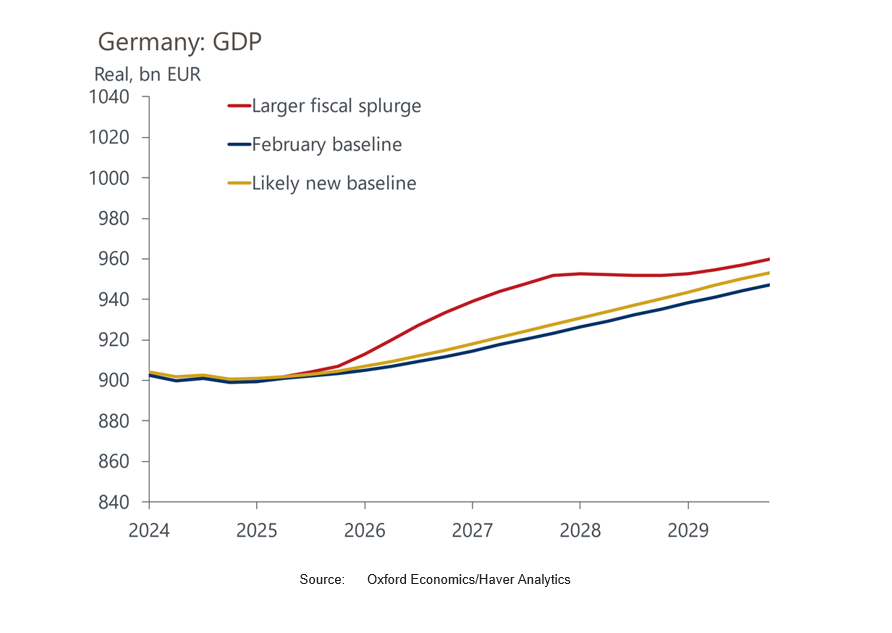

- Nonetheless, even a partial use of the additional fiscal space presents a material upside to our previous baseline, and supports the changes we have made in our latest forecast. We now expect deficit to double over the coming years to 1.5% of GDP to finance a hike in defence spending to 3% of GDP. We think that will lift the level of GDP around 0.6% above baseline by 2029 and raise Bund yields by 20bps to 2.65%.

- In a scenario with a big infrastructure splurge and an even larger and more front-loaded rise in defence spending GDP could be 1.4% above baseline by 2029 But the economy would likely struggle to scale up defence and infrastructure capacity that quickly. So delays to projects, a marked rise in inflation, and a subsequent monetary policy response are likely.