Research Briefing

| Feb 21, 2025

Japan’s small firms’ profitability will help determine further rate hikes

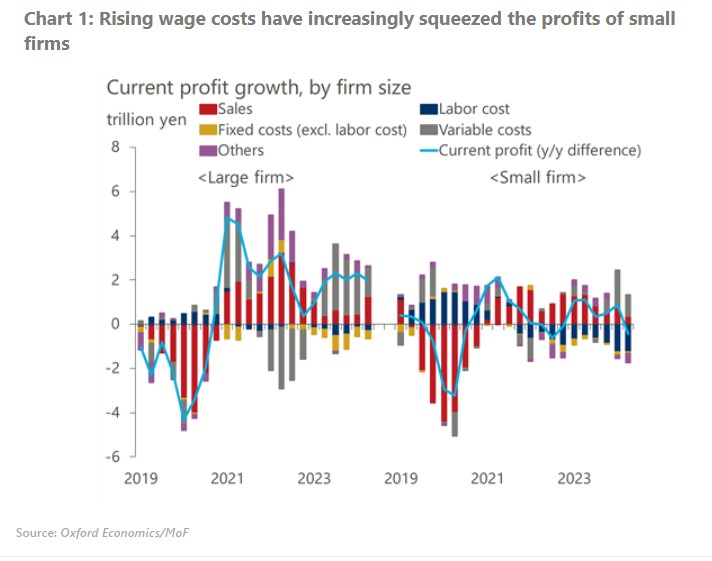

Rising wage costs have been increasingly squeezing the already low profitability of small firms in Japan, thereby raising concerns about the sustainability of the wage-driven inflation dynamics. The evolution of these dynamics will be key in determining how far the Bank of Japan can raise its policy rate in the coming years.

What you will learn:

- The profitability of small firms has remained almost flat despite their efforts to raise sales by passing on rising costs to prices. Lacklustre consumption has restrained their pricing power and their productivity growth has remained stagnant. Small firms have higher wage costs as a percentage of sales and low profitability makes them vulnerable to projected rate hikes.

- We project small firms will manage to keep pace with the wage increases set by leading large firms this year. However, given the wide variation in the profitability of small firms, more unprofitable firms will likely start to fall behind the overall wage growth trend. The BoJ will take time to examine wage rises in small firms before possibly hiking the policy rate in July.

- In the coming years, we project the wage gap between large firms and small firms will widen. Risks to the capacity of small firms to follow the overall pace of wage growth are tilted to the downside. Major risks to our outlook are disappointing growth in consumption and a persistent rise in import costs due to external shocks, including further yen weakening.