Research Briefing

| Mar 16, 2023

Japan: Incoming Governor Ueda is entrusted to tweak the YCC

At Governor Kuroda’s final policy meeting, the Bank of Japan (BoJ) left short-term policy rates at -0.1% and long-term rates at around 0%. Despite mounting pressures on the 10-year JGB, the target range was kept at +/-0.50ppt.

While we did not discount the possibility of a widening of the band to secure a smooth leadership transition, Kuroda appears to have avoided a sharp rise in JGB yields before the end of the fiscal year. In particular, further losses in the domestic bond portfolio threaten the profitability of the already vulnerable regional banks.

What you will learn:

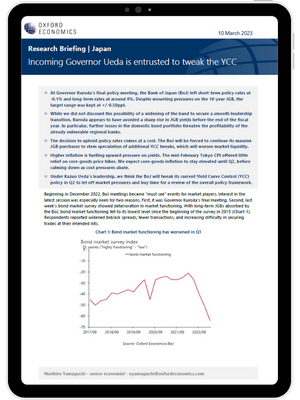

- The decision to uphold policy rates comes at a cost. The BoJ will be forced to continue its massive JGB purchases to stem speculation of additional YCC tweaks, which will worsen market liquidity.

- Higher inflation is fuelling upward pressure on yields. The mid-February Tokyo CPI offered little relief on core-goods price hikes. We expect core-goods inflation to stay elevated until Q2, before calming down as cost pressures abate.

- Under Kazuo Ueda’s leadership, we think the BoJ will tweak its current Yield Curve Control (YCC) policy in Q2 to let off market pressures and buy time for a review of the overall policy framework.