Industrial spending to drive Australian maintenance activity to new highs

Australian maintenance expenditure is forecast to average a record $54.5bn over the five years to FY27. We define maintenance as “work undertaken on an asset which improves the standard and/or quality of the asset but does not improve on the original design standard.”

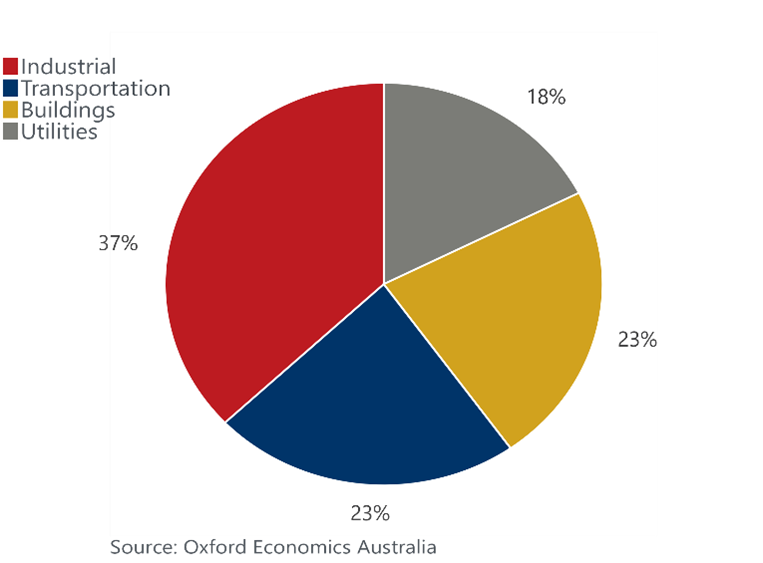

Chart 1: Sectoral composition of maintenance spending for FY23

The industrial sector, which includes mining and manufacturing, is the largest category, accounting for 36% of domestic maintenance spending over FY22. Increasing maintenance requirements of major LNG facilities will ensure that this sector remains the fastest growing over the coming years. Mining maintenance spending more generally will be supported by increasing production following China’s reopening, although there are risks that China’s emission targets could weigh over global demand for metals. Activity for the manufacturing sector is set to grow, albeit at a slower rate, as government programs continue to support the sector.

Transportation maintenance spending is dominated by road maintenance activity. Spending jumped following covid lockdowns as the federal government looked to shovel ready projects to stimulate an infrastructure led recovery. The 2022 east coast floods added to this boom, driving national transportation maintenance work to a record high. Spending is now set to normalize, although there remains significant upside risk to the outlook should flooding occur in population centres, or an economic slowdown drive another wave of government stimulus. Over the medium to longer-term government investment in road and railway infrastructure will increase maintenance requirements.

The outlook for utilities is more subdued. The transition to renewable electricity generation will see coal and gas power stations replaced by wind and solar generators, which have much lower maintenance requirements. Furthermore, the next phase of the NBN expansion will see more of the copper network replaced by fibre, which is also much less costly to maintain. Slow, and at times negative growth in both sectors will lead to a more subdued outlook for total utility maintenance activity.

Growth in non-residential building maintenance spending is expected to remain solid, with work on health and education buildings being the key driver of activity. Defense building maintenance work will also continue to grow as the post-covid backlog continues to be worked through.

Record high levels of maintenance activity are coming at a time when domestic non-oil and gas construction activity is also at record highs. Maintenance requires similar materials and skills to construction activity, and thus further adds to capacity constraints and cost pressures facing the industry. While the federal government is reassessing the delivery of the national infrastructure pipeline, maintenance spending is not as easy to defer. Operators and suppliers can therefore look to the maintenance market to prepare for the future slowdown in construction work.

To learn more about Australian maintenance outlook, download our MAINTENANCE IN AUSTRALIA 2023 EDITION here.

Authors

Tags: