Research Briefing

| Aug 2, 2024

How our FX risk tool helps predict exchange rate sell-offs

The latest revamp of our foreign exchange risk tool (FXRT) demonstrates the enhanced predictive power of selected vulnerability metrics over future exchange rate movements. Our newly updated weights show that scores explain around 40% to 60% of y/y nominal bilateral exchange rate movements in a panel of 157 currencies from 2000 to Q1 2024.

What you will learn:

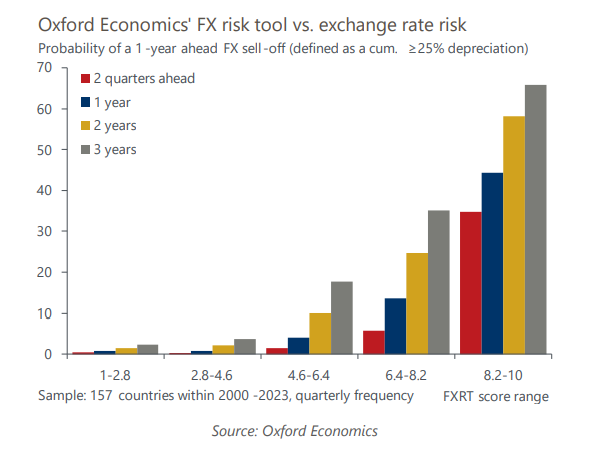

- On a global level, the FXRT scores help highlight the currencies most susceptible to extreme FX movements. Our backtests show that nearly two-thirds of currencies within the riskier score range experienced a 25% or higher sell-off within the next three years.

- We find that conditional distribution skews pair well across scores. Riskier currencies according to the FXRT tend to have more prominent negative skews, consistent with the view that once fundamental vulnerabilities are exposed, negative sentiment becomes amplified. The revisions suggest increases in the FX risk for the Japanese yen and the Swedish krona.

- Our risk scores are useful to inform policy or financial market strategy decision-making. They are also beneficial quantitative inputs to inform other in-depth analyses in the context of econometric models focussed on exchange rate research.

Related Reports

Click here to subscribe to our asset management newsletter and get reports delivered directly to your mailbox

Czech Republic: Profligate fiscal loosening will push up bond yields

We think the Czech 10-year bond yield is on track to breach 5% in the coming months, as the markets continue to price in the fiscally profligate programme of the new government.

Read more: Czech Republic: Profligate fiscal loosening will push up bond yields

Why bond yields are rising again and why it matters

The rise in bond yields reflects fiscal concerns, higher risk premia, shifting investor preferences, and idiosyncratic factors.

Read more: Why bond yields are rising again and why it matters

Indirect climate risk in financial analysis

Climate and other sustainability challenges can affect the finance sector and have a material impact on returns to capital.

Read more: Indirect climate risk in financial analysis

Economics for Asset Managers

Read more of our analysis and reports on asset management and economic outlook.

Read more: Economics for Asset Managers