Research Briefing

| Feb 14, 2024

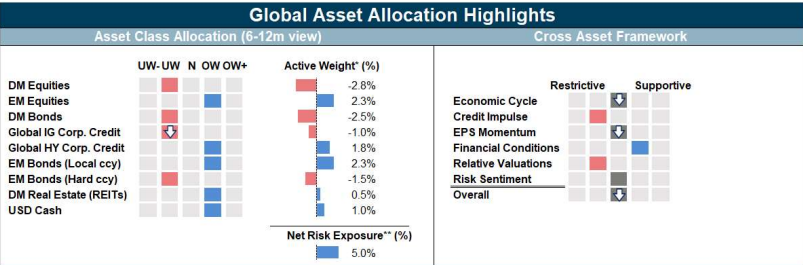

Cross Asset: Sticking with our risk on tilt as the growth outlook improves

We remain modestly risk-on as our above-consensus view on US growth this year still favours risk assets over bonds.

What you will learn:

- We think the soft landing we forecast is unlikely to translate into a strong EPS recovery and we therefore prefer high-yield credit over DM equities. Credit has a lower sensitivity to swings in earnings growth and resilient balance sheets mean we are constructive on the corporate default cycle.

- We are overweight cash and underweight long duration assets including DM bonds, IG corporate and EM sovereign credit. Our soft-landing view for the global economy and elevated coupon issuance over the coming quarters favours the shorter duration segment of the curve.