Research Briefing

| Jul 26, 2024

Closing our short SEK trade to capitalise on the Scandi FX sell-off

As we head into the summer recess where central bank meetings are few and far between, we capitalise on seasonal illiquidity and the extraordinary sell-off in Scandinavian FX by closing out our long EURSEK trade, opened in May. Our view was primarily driven by our more aggressive rate forecast than the consensus. As of today, however, the market has moved in our direction.

What you will learn:

- We expected a bout of SEK weakness following the Riksbank rate cut in the spring, but we think the recent sell-off is overdone, and we close our long EURSEK trade, opened in May.

- With the worst now behind us, we now think rates are unlikely to re-price lower. We are less sanguine than the market’s expected 150 bps of cuts over the next year – the steepest cutting cycle in G10, bar New Zealand – and we remain underweight Swedish bonds in our fixed income allocations.

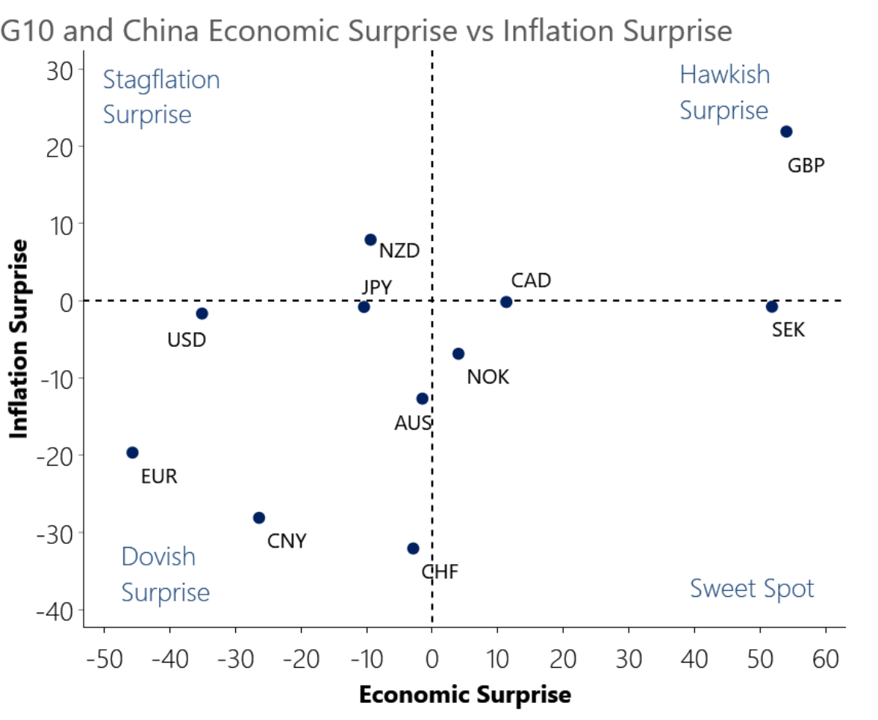

- Our FX scorecard does not show a low ranking for SEK, based on valuation drivers in particular, and we think it opportune to close our short SEK position for a modest profit.

Related Reports

Click here to subscribe to our asset management newsletter and get reports delivered directly to your mailbox

Czech Republic: Profligate fiscal loosening will push up bond yields

We think the Czech 10-year bond yield is on track to breach 5% in the coming months, as the markets continue to price in the fiscally profligate programme of the new government.

Read more: Czech Republic: Profligate fiscal loosening will push up bond yields

Why bond yields are rising again and why it matters

The rise in bond yields reflects fiscal concerns, higher risk premia, shifting investor preferences, and idiosyncratic factors.

Read more: Why bond yields are rising again and why it matters

Indirect climate risk in financial analysis

Climate and other sustainability challenges can affect the finance sector and have a material impact on returns to capital.

Read more: Indirect climate risk in financial analysis

Economics for Asset Managers

Read more of our analysis and reports on asset management and economic outlook.

Read more: Economics for Asset Managers