Research Briefing

| May 7, 2024

Central banks edge towards a tipping point for rates

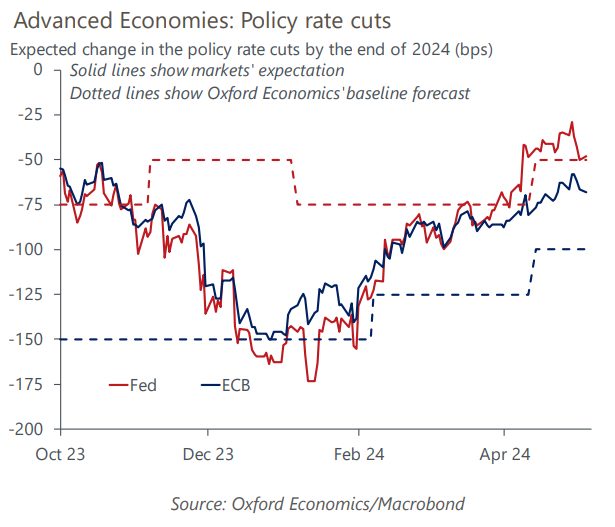

After getting carried away at the turn of the year with the likely extent of Federal Reserve rate cuts in 2024, markets recently have swung too far in the opposite direction. We still expect the Fed to cut rates by 50bps this year and the European Central Bank by 100bps.

What you will learn:

- High inflation and uncertainty over the future pace of decline means that policymakers will reduce interest rates with caution. Nonetheless, we expect core inflation in the US and eurozone to have eased by Q3 to rates associated with the policy rate cuts in the past.

- The US economy is still growing at a healthy pace and the eurozone has resumed growth, but during past cutting cycles, central banks have rarely waited for recessions before cutting policy rates.

- Still, policymakers may need some kind of trigger to actually cut rates. A potential catalyst is a desire to lower rates from a risk-management perspective.

- We think that markets are overestimating how much the Fed will constrain policy rate cuts by the ECB. Central banks typically do not begin cutting or tightening cycles at the same time, and we do not see why this time will be different. The ECB currently has a tighter policy stance than the Fed and can be more confident than the Fed that core pressures will continue to ease. As a result, the ECB can pivot to rate cuts more boldly and earlier than the Fed.