Research Briefing

| Sep 9, 2024

Asia Pacific: Summertime blues foreshadow the slowdown

Four themes have dictated Asia’s macroeconomic outlook over the summer and are likely to continue to exert an influence over the rest of the year and into 2025, in our view.

What you will learn:

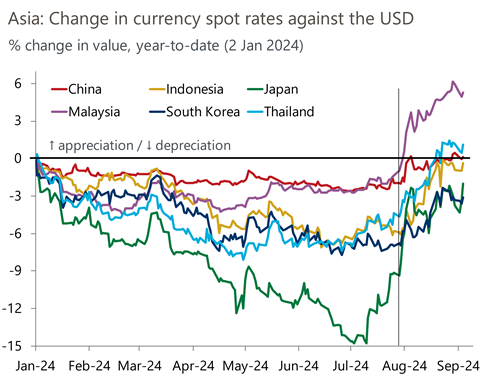

- The first is the financial market volatility we saw in early August that has resurfaced this week. Among other concerns, worries are building that growth in the US could slow by more than what financial markets had discounted, and that the Federal Reserve may have waited too long to cut rates and slipped ‘behind the curve’. We look at how that could affect Asia.

- Second, we have now received Q2 growth data from across Asia. While not apparent from year-on-year numbers, a closer look indicates that the growth slowdown may already be upon us. What’s more, it looks unlikely that aside from the current boost from AI, Asia has an engine of growth to rely on.

- Third, given a cut in the Fed Funds rate is imminent and that Asian central banks’ usual reaction is to follow the Fed, we ask will this time prove the exception? We think three central banks – India, Malaysia, and Thailand – are unlikely to be moved. We examine the reasons for the exceptionalism and the likely monetary stance in those countries.

- Fourth, in China the tussle between a structural slowdown and cyclical policy support seems to be going the way of the former. Growth in Q2 was worse than expected and a turnaround appears unlikely. Exports are doing well, but that strength is unlikely to endure.