Research Briefing

| Nov 20, 2023

A weaker dollar hinges on better global growth prospects

The dollar will continue to be supported by a high carry and the relative resilience of the US economy. Even the recent loosening of financial conditions – itself based on the pullback in yields and a more flexible Fed – have only partially dented the USD bullish trend.

What you will learn:

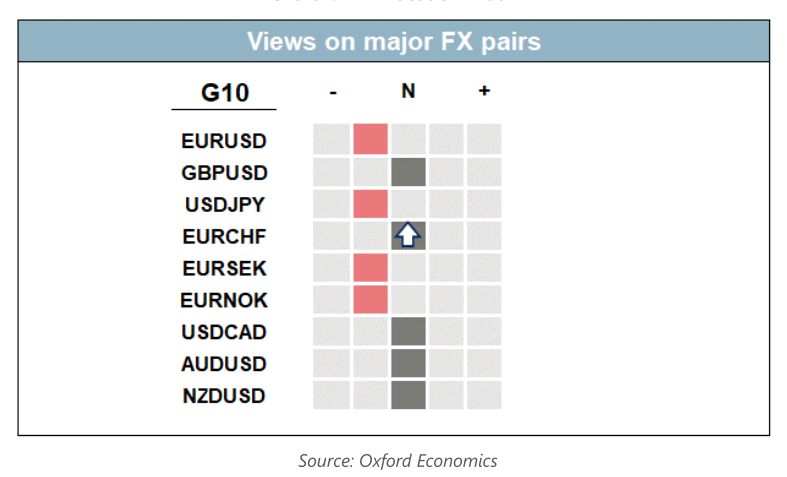

- We do not expect major policy shifts heading into year end and given the broad similarity of G10 rate cutting cycles that are priced in, we expect range trading behaviour across major US dollar crosses in the near term.

- The greenback is overvalued fundamentally, but 2024 will disappoint dollar bears. The pivot the market expects on the back of weaker data and continued benign disinflation – in part driven by lower commodity prices – will take time to materialise.

- Our first rate cut is after the summer of 2024, leaving the US with still elevated short-term real rates. Worsening global liquidity will also be USD-positive in 2024, except against the yen. The latter is poised to outperform major cyclical G10 (GBP, AUD and CAD) crosses in 2024.