US-Iran war: Construction cost impacts to linger

Falling oil prices offer some relief, but higher labour costs, material prices, and supply chain risks are likely to persist.

US-IRAN WAR: CONSTRUCTION COST IMPACTS TO LINGER

The ceasefire provides some optimism, but not immediate relief, for Australian construction costs.

The memorandum of understanding (MoU) between the United States and Iran has raised hopes that the conflict is moving toward resolution. On the face of it, the MoU extends the ceasefire by 60 days, reopens the Strait of Hormuz and lowers the immediate risk of a prolonged energy shock, offering a welcome easing in both geopolitical and market tensions.

For Australia’s construction industry, however, the cost story is more complicated. Energy prices can move quickly as geopolitical risks rise or fall, but construction costs do not reset overnight. Infrastructure damage could keep energy prices elevated for longer, while other pressures may already be embedded in wage negotiations, tender allowances and project budgets.

That means the ceasefire matters, but it does not immediately remove the oil premium from Australian construction. The key issue is not just whether fuel prices fall from here. It is how much of the shock has already flowed through the system, how much of it will prove sticky, and how exposed the sector remains if the current diplomatic progress fails to hold.

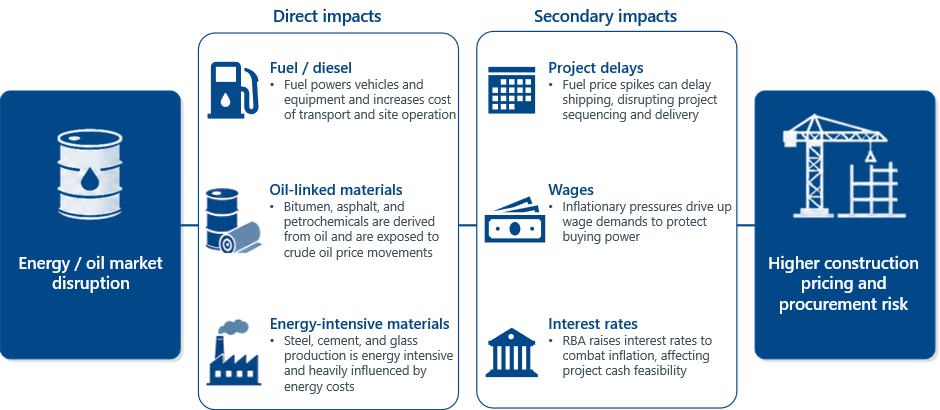

Energy shocks matter to construction because the sector is highly exposed to oil and energy markets in several ways, and more so than most other sectors.

The most direct effects arise through higher costs for refined oil products used in construction. These include the fuel used to power vehicles and equipment, oil-based materials (such as bitumen, plastics and resins), and materials that use energy-intensive production processes (such as steel, cement, and glass).

There are also second-round impacts. Conflict-related disruptions can delay shipments of key construction materials, interrupting project sequencing and delivery. That matters because construction projects continue to incur preliminary and overhead costs even when work slows or stops. Higher energy prices can also add to broader inflation, which can feed into negotiations and interest rates, and raise project feasibility hurdles.

The pass-through is already visible in input prices most directly exposed to oil markets.

Using the latest available June-quarter pricing indicators, Australian diesel prices were approximately 50% higher than in the previous quarter[1]. Bitumen tells a similar story, with June quarter prices around 34% higher than in the March quarter across Queensland[2], Victoria[3], and Western Australia[4].

These inputs represent a meaningful share of project costs. As a broad guide, diesel and road freight account for around 5% of total costs on a typical infrastructure project. For road projects, the combined share of diesel and bitumen can exceed 20%.

While crude oil prices can fall quickly when energy markets calm, damage to energy infrastructure means prices may take longer to return to pre-conflict levels.

A defining feature of the conflict has been the direct impact to energy infrastructure across the Gulf. Qatar’s LNG capacity has been largely shut down at the Ras Laffan industrial hub, while fires and operational issues have been reported at Saudi Arabia’s Ras Tanura refining complex and energy installations in Fujairah, UAE.

Reactivating a refinery after a forced shutdown requires a phased restart to ensure operational safety and equipment integrity which can take up to several weeks to resume. Repairs can take longer still, depending on the extent of the damage.

The bottom line is that attacks on refineries and processing infrastructure could prolong market disruption more than crude shortages alone. Even if a reopening of the Strait of Hormuz will “let the oil flow!”, energy prices may remain elevated while damaged infrastructure is repaired and normal operating capacity is restored.

Other construction costs may be even slower to adjust.

Wages are the clearest example. Higher energy prices can feed through into broader inflation, raising the cost of living and increasing pressure for wage growth across the economy. Once wage outcomes are agreed, they rarely reverse. At best, they tend to plateau. In construction, many wage outcomes are also locked in for several years through enterprise agreements and awards, meaning higher labour costs can persist even after the original energy shock has faded.

The exact same logic applies to procurement. Some projects may have already committed to materials, equipment or subcontract packages at prices that reflected the higher-risk environment. If these costs are locked in, lower energy prices will take time to flow through.

Risk pricing can also prove sticky. Contractors, suppliers and project financiers are unlikely to remove contingencies immediately after conditions improve, particularly if recent volatility has made input costs harder to predict. If higher energy prices have also contributed to broader inflationary pressures, financing costs may remain elevated for longer.

What happens if the conflict drags on?

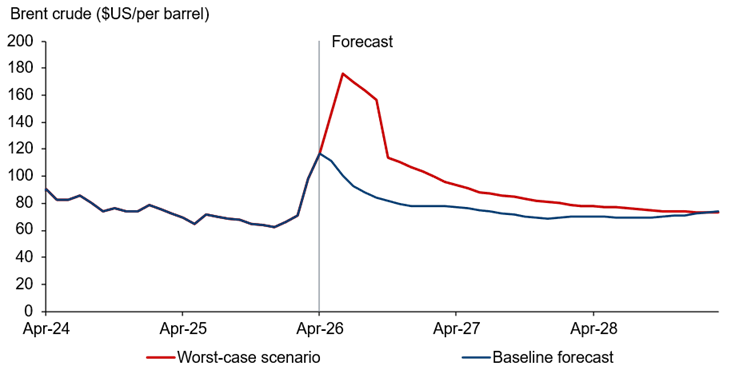

At Oxford Economics Australia, we have analysed the conflict and the potential impact under different scenarios in depth. Our baseline scenario assumes trade flows begin to recover gradually between July and September this year, before returning to normal by March 2027. A more severe downside scenario pushes this recovery back by around six months and factors in further damage to key infrastructure.

In that downside scenario, Brent crude oil prices rise to significantly higher peaks and remain elevated for much longer, not returning to normality until at least 2029.

The reason is that today’s supply-chain buffers are limited. So far, global supply chains coped relatively well, all things considered. Trade routes have been reconfigured, reserves have been drawn down, and alternative suppliers have helped limit the scale of disruption. Resin exports are a useful example. With production constrained in Gulf countries, China has been able to step in by importing feedstock from US and Russian reserves, helping to prevent a sharper escalation in prices.

But these reserves are limited. Under the baseline forecast, where an end to the conflict is in sight, this might be manageable. Under a prolonged conflict, continued uncertainty and further infrastructure damage would place greater strains on supply chains, delaying the recovery in trade flows and keeping oil-linked cost pressures elevated for longer.

The key issue is exposure, not just the price of oil.

The MoU is an important step in reducing the immediate risk of a prolonged energy shock. But for Australia’s construction sector, the cost story will not end when oil prices start to fall. Some costs will respond quickly. Others have already been written into wage agreements, procurement decisions, subcontract packages and risk margins.

That makes exposure the practical issue for clients and contractors. Projects with greater reliance on oil-linked products will remain more vulnerable to lingering cost pressures. Smaller subcontractors may also face greater pressure where costs rise after prices have already been agreed.

The ceasefire may reduce the size of the shock, but it does not erase the pass-through already in the system. For construction, the question now is not only whether energy prices normalise. It is where higher costs have already been locked in, and how long they will take to unwind.

[1] Australian Institute of Petroleum, “Pricing”, June 2026

[2] Queensland Department of Transport and Main Roads, “C170 Bitumen Prices”, May 2026

[3] Victorian Department of Transport and Planning, “Construction Works and Services – Tenders and Contracts”, June 2026

[4] Western Australia Main Roads, “Rise and Fall – Bitumen Index”, June 2026

Contact us

Complete this form and we will contact you to set up your free trial. Please note that trials are only available for qualified users.

We are committed to protecting your right to privacy and ensuring the privacy and security of your personal information. We will not share your personal information with other individuals or organisations without your permission.