Industry will be ground zero for disruption caused by Trump’s North America tariffs

President Trump’s decision to impose 25% tariffs on all non-energy goods from Canada and Mexico, and a 10% tariff on energy goods from Canada, represents a drastic break from the economic status quo and is paving the way for significant disruptions for industrial sectors across North America. Tariff-induced price increases call into question tightly integrated supply chains across the continent and make large swathes of exports less competitive.

The potential fallout from these tariffs is significant. While the overall impact on GDP may not be catastrophic, industry as a whole will be hurt more, and certain sectors could suffer greatly. Various industries in Mexico and Canada are particularly exposed given their size relative to the US and their reliance on US markets, in terms of both demand and supply. Moreover, in the US, while industry is proportionately much less exposed in terms of final demand and supply chain reliance, parts of its industry are certainly highly interconnected to its neighbours and thus may see input price spikes or supply chain disruptions.

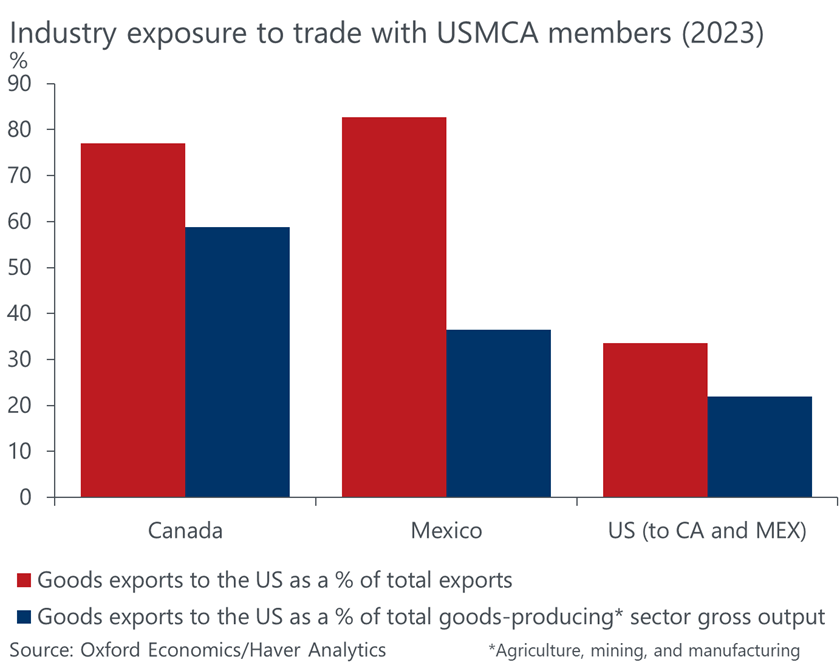

Canadian and Mexican industry have a lot more to lose

In Canada, industries such as mining, motor vehicles, basic metals and machinery face considerable risk. These sectors rely heavily on exports to the US: the value of exports to the US for each of these industries is over 60% of their gross output, which is roughly equivalent to total sales. Our estimate for the median sector, textiles & clothing, is just over 40%, and even the least-exposed sector, non-metallic minerals (which produces goods like cement and glass), has a value of 11%. There is no industrial sector where the share of exports as a proportion of total production appears trivial—a large share of demand for will be rendered less competitive by these tariffs.

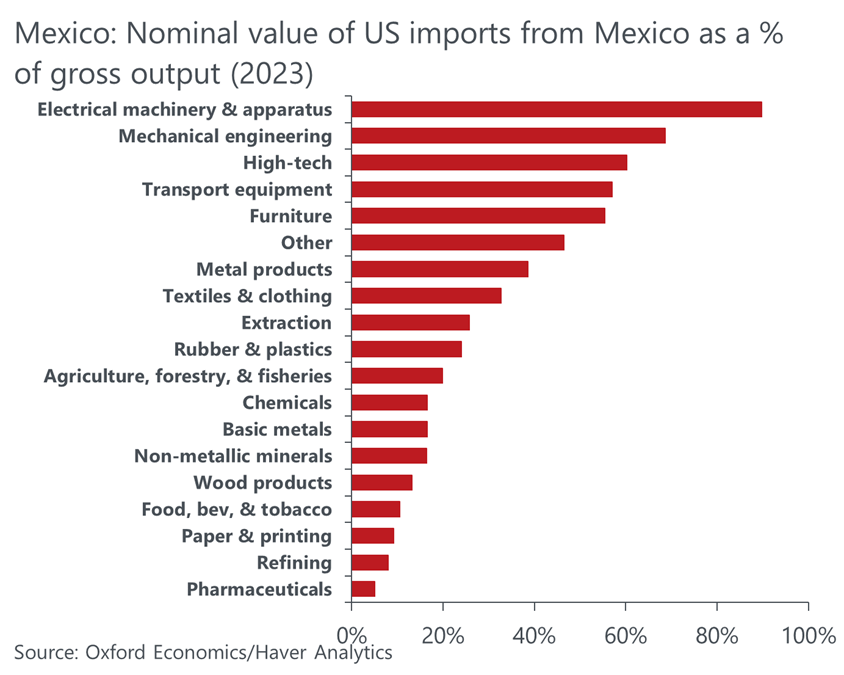

The situation is similar in Mexico, where our estimates suggest that exports to the US are valued at more than half of the value of gross output of electricals (90%), machinery (69%), high-tech (60%), furniture (55%), and transport equipment (57%). The degree of exposure through the demand channel is somewhat lower for the median sector than in Canada (rubber & plastics at 24%), and there are a few sectors where the degree of demand exposure is in the single digits (pharma, refined energy products, and paper & printing).

Unlock exclusive economic and business insights—sign up for our newsletter today

Supply chain vulnerability is asymmetrical

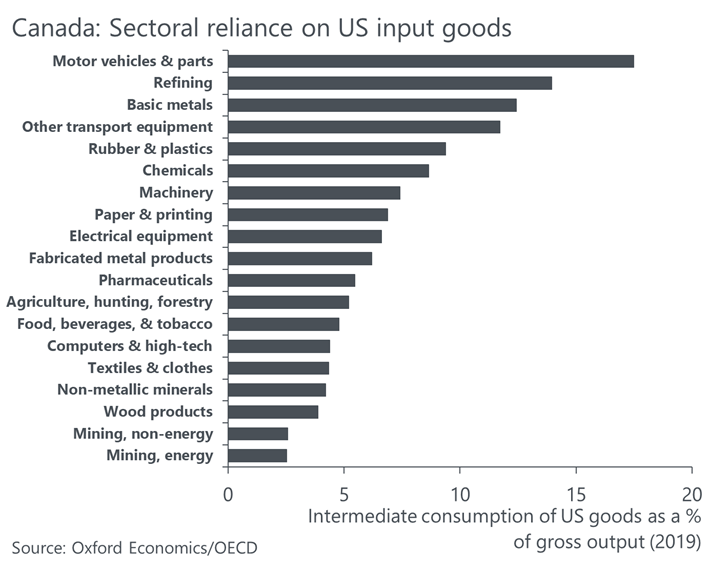

Another key point of vulnerability for Mexico and Canada is their broad-based degree of supply chain reliance on the US. In Canada’s industrial sectors, the value of US-made intermediate inputs accounts for between 3% and 17% of the total, while in Mexico the comparable range is from 3% to 15%. Transport equipment (particularly automotive), basic metals, rubber & plastics, chemicals, electricals and machinery stand out with above-average reliance on US inputs in both countries.

These sectors would see a secondary round of challenges, beyond the demand impacts addressed above, if their governments were to impose retaliatory tariffs that increased costs of goods coming into Canada and Mexico. This would raise their input costs and further undermine their competitiveness. However, it should be noted that the degree of retaliation by Canada and Mexico is, as of writing, unclear, and it is possible (if not likely) that they will avoid actions that could hurt their own industry.

US industry exposure from tariffs is more limited, but motor vehicles at the top of the list

We think a key reason why President Trump feels able to impose these tariffs is that the risks to US industry are far more limited—the vast domestic market allows the US to weather trade shocks better than Canada or Mexico. This is true both on the demand side, where exports to Canada and Mexico make up a much smaller chunk of industry’s total output, and on the supply chain side, where imports of intermediate inputs make up a much smaller chunk of the value of final production. Indeed, US industry is relatively more autarkic: about 85% of the inputs used in goods production come from within the US, and only about 4% of the value of final production comes from inputs from Mexico and Canada.

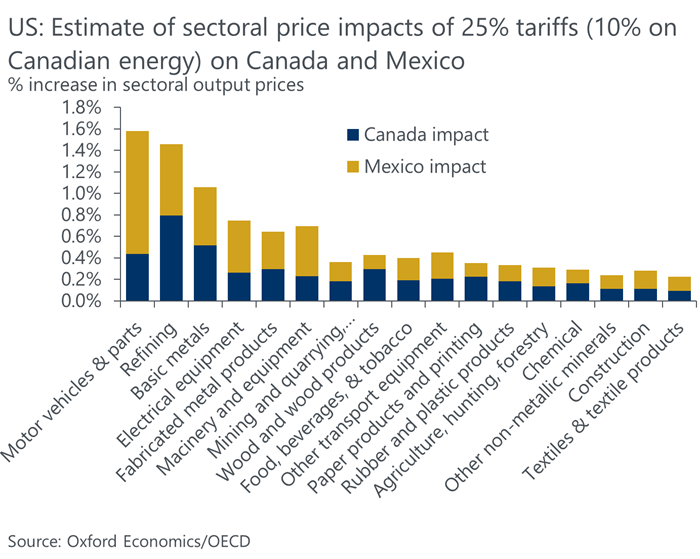

However, certain sectors, particularly motor vehicles, could still feel the pinch. Our research indicates that a 25% tariff shock could have a more pronounced impact on automotive: producer prices for the sector would increase more than two times as much as the median industrial sector. It is also possible that this is an underestimate, as the interconnected nature of this sector means that inputs often cross borders more than once before final assembly. Tariffs would be imposed each time this happens. This could result not only in price increases, but also potentially production shutdowns if the effect is such that production lines become financially unviable.

The exemption of Canadian energy from the 25% tariff rate represents a key recognition by the President that energy is one of the other key areas of vulnerability for the US. Of US crude oil imports, 56% come from Canada. The EIA estimates that in 2023, Canadian imports of crude and finished oil products accounted for about 22% of total US petroleum consumption in the US. Imposition of a tariff of 10% (rather than 25%) is a recognition that energy prices in the US are quite dependent on Canadian supply. A 10% rate will increase prices, but certainly by less than the full 25% would have.

For a more detailed analysis, download our Industry Research Briefing.

More to come?

We are currently updating our macroeconomic and industry forecasts to reflect the imposition of these tariffs. Our macroeconomic forecasts, which will show a notable economic hit to the Canadian and Mexican economies and a moderate hit to the US (though with increased inflation due to tariffs on consumer goods like Mexican fruit & vegetables) this year, will be released in the coming days. Our comprehensive sector-by-sector forecasts released as part of the Global Industry Service will be available in early March. If you’d like to request a trial of the service, please feel in the form below.

Request a trial

Tags: