Research Briefing

| Aug 18, 2022

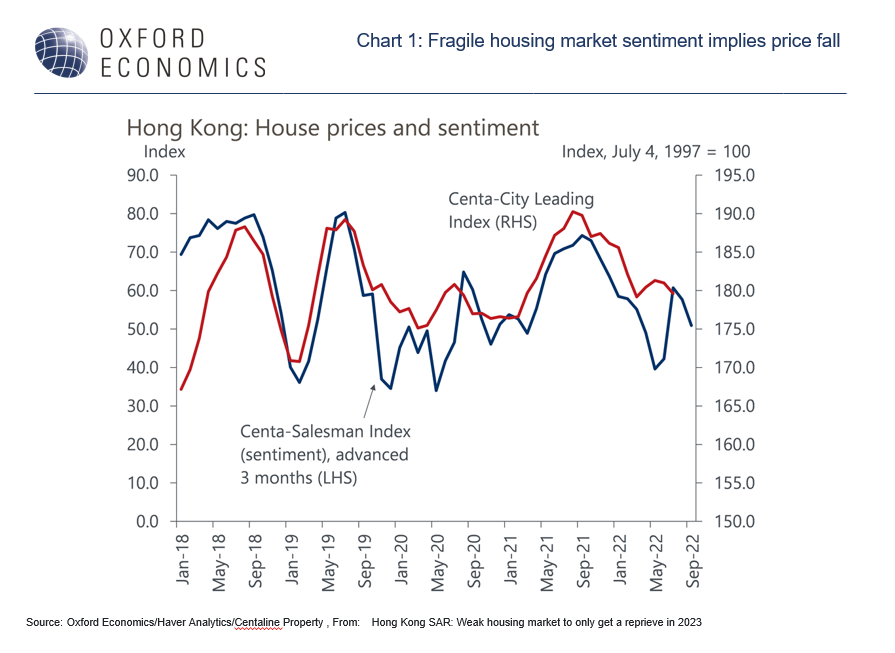

Hong Kong’s weak housing market to only get a reprieve in 2023

Hong Kong’s housing market sentiment weakened during H1 2022, reflecting a resurgence of Covid infections in Q1 and a weak domestic economic outlook. House prices in the secondary market fell 2.8% in Q2 versus Q4 2021. And this housing market weakness may not be over yet.

What you will learn:

- As an international trade and financial centre in Asia, changes in Hong Kong’s external environment have an

outsized impact on its domestic economy, and hence on its housing market. - We expect residential property prices to fall by about 4% y/y in Q4 2022, mainly due to the gloomy economic outlook. Slow border reopening progress and challenges to the external environment have severely dampened local sentiment.

- Higher mortgage rates will also play a role in deterring lower income households from buying property and weigh on residential property investment demand.