Healthy tech spending set for growth in Asia Pacific, but the road ahead is rocky

- APAC is expected to outpace both Europe and the US in terms of spending in 2024 and 2025, and it is projected to be responsible for more than half of the global 1.7 ppts acceleration in spending growth next year.

- Despite potential opportunities, risks remain. Our global macro scenarios indicate that risks are generally skewed to the downside. Not only is the APAC region exposed to high cyclicality of demand for chips, but the boost from AI adoption might not be as fruitful as anticipated.

Spending on tech is a key way in which Asia Pacific (APAC) countries can foster their economic growth by contributing to innovation, resilience, and international competitiveness. The APAC region has certainly cemented itself as the global powerhouse of tech spending. But while we forecast that this trend will continue, we have also identified risks that business leaders will need to address.

APAC to lead the growth in tech spending

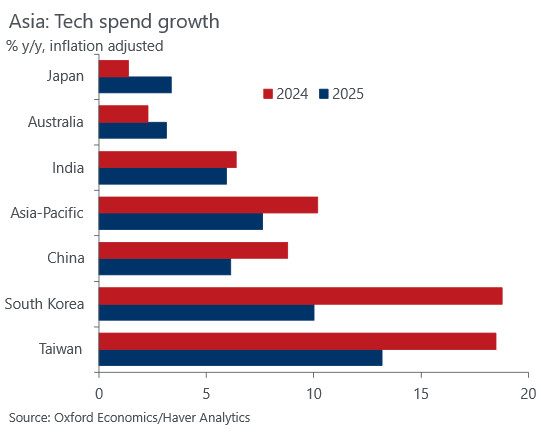

APAC is expected to outpace both Europe and the US in terms of spending in 2024 and 2025, and it is projected to be responsible for more than half of the global 1.7 ppts acceleration in spending growth next year. And although we forecast that expenditure will decline from 2024 to 2025, from 10.2% to 7.6% respectively, growth will still be robust and double the pace of GDP in the region. The economies forecast to see the largest growth in tech spending in 2024 are Taiwan (13.2%), South Korea (10%), and China (6.1%), and the main reason for this is semiconductors (Chart 1).

Chart 1: Slowdown in 2025, but the leaders still in topping the table

Semiconductors are the foundation of modern technology, and they are used in everything from mobile phones to cars to household appliances to banking. They can pack billions of transistors into one, small chip, and have replaced older vacuum tubes to make devices smaller, faster, and more efficient. Considering their widespread application, we expect the global sales to reach a total value of US$599 billion by the end of 2024. And, as the main APAC producers of semiconductors, it also explains why Taiwan, South Korea, and China are set to lead tech spending now and in the future. But this can be a double-edged sword.

Unlock exclusive economic and business insights—sign up for our newsletter today

Asia is a large producer of electronics, and the region’s spending is mainly via the operating expenditure channel, which means spending in this area often reflects demand elsewhere. This demand, in turn, is cyclical, leaving companies exposed to the ebbs and flows of the business cycle. And the demand is originating from somewhere else, meaning that supply chains must remain robust for companies to keep producing and innovating without disruptions—Covid-19 serves as a stark reminder of what can happen when these chains fail.

Risks from AI, protectionism, and politics

Despite our forecasts for overall healthy growth in 2025, there are risks ahead. Not only is the APAC region exposed to demand for chips, but the boost from AI adoption might not be as fruitful as anticipated. In addition, with geopolitical tensions rising, further protectionist policies and instabilities loom over the horizon; the full impact of the continued technological decoupling of the US and China has yet to be felt. Our global macro scenarios indicate that risks are generally skewed to the downside. The higher for longer interest rate scenario poses the largest threat to most countries in the region. Still, the Harris victory scenario (in the upcoming US election) and the inflation victory scenario are both expected to contribute to more tech spending in most countries examined, relative to our central forecast.

In today’s dynamic environment, having insights into global tech spending across industries will allow businesses to manage the risks ahead. The Global Tech Spend Forecasts—our new proprietary solution for analysing enterprise spending on technology across 25 economies, accompanied by global and regional composites—allows our clients to make informed, strategic decisions based on spending data and forecasts. And our coverage here includes key subsectors such as devices, enterprise software, IT services, internet and cloud services, and communication services, ensuring comprehensive insights that help our clients unlock the potential of economics to create successful growth strategies.

Tags: