Research Briefing

| Jun 27, 2024

亚太地区: 2024 年亚太地区城市的消费支出将保持温和增长

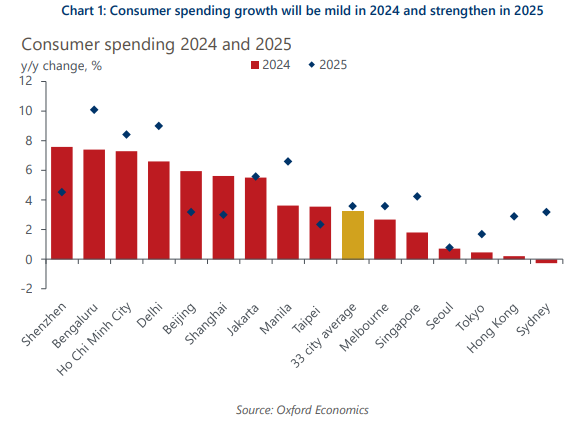

我们预测 2024 年亚太地区城市的 GDP 增长将放缓,平均降至 3.3%。 持续的通货膨胀和劳动力市场的日益疲软将拖累收入,进而影响消费支出的增长。 低迷的消费者信心反映出消费者的风险规避情绪,这进一步表明今年亚太地区城市的消费支出疲软。 2025 年,随着上述影响的减弱和全球经济翘尾因素的增强,经济增长速度将恢复加快。

你将了解到什么:

- 悉尼和首尔等几个亚太地区城市的通胀率下降速度比最初预期的要慢。 我们预计,在整个 2024 年,这些城市持续的价格压力将拖累消费者的消费能力。

- 经济增长放缓可能会导致亚太地区多个城市的劳动力市场更加疲软。 我们预测,新加坡和悉尼等地的失业率将上升,导致实际收入负增长和消费支出增长放缓。

- 亚太地区各城市消费者信心低迷,进一步印证了我们的观点,即今年亚太地区各城市的消费支出将保持温和态势。 我们认为,消费者今年将采取 “规避风险 ”的态度,一般不会进行大额消费。

牛津经济研究院 (Oxford Economics) 是全球领先的独立经济预测及量化分析机构。基于领先的全球经济分析及行业分析模型,我们提供覆盖全球200多个经济体、100多个行业板块和8,000多个城市和地区的经济研究报告、预测及分析工具;并能够协助客户对市场走向进行预测,分析其对于经济、社会及商业的影响,为客户制定决策奠定坚实基础。