Research Briefing

| Feb 21, 2024

UK: Housing market on course for a soft landing

The recent sharp fall in mortgage rates and continued strong growth in wages has significantly reduced the scale of the UK’s housing affordability problem. Consequently, the risk of a steep correction in house prices is much lower than it appeared a few months ago. We also expect the recent steady pickup in housing market activity to continue.

What you will learn:

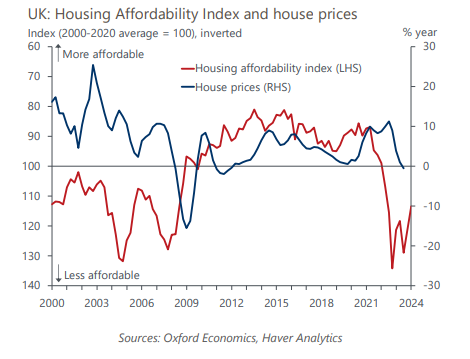

- Our Housing Affordability Index, which is based on the affordability of mortgage payments, suggests that house prices are currently 14% overvalued. This is down from 29% last summer.

- Though existing mortgagors needing to refinance this year still face a marked increase in debt servicing costs, the average uplift is now likely to be just under 200bps. Had mortgage rates stayed at their Q3 2023 levels, the average increase would have been 330bps.

- We now expect house prices to fall just 4% from peak-to-trough, a far smaller drop than in previous cycles. But such a shallow cycle would leave valuations still very stretched, limiting the scope for strong price growth in the recovery and keeping activity below historical norms.