Research Briefing

| Aug 1, 2024

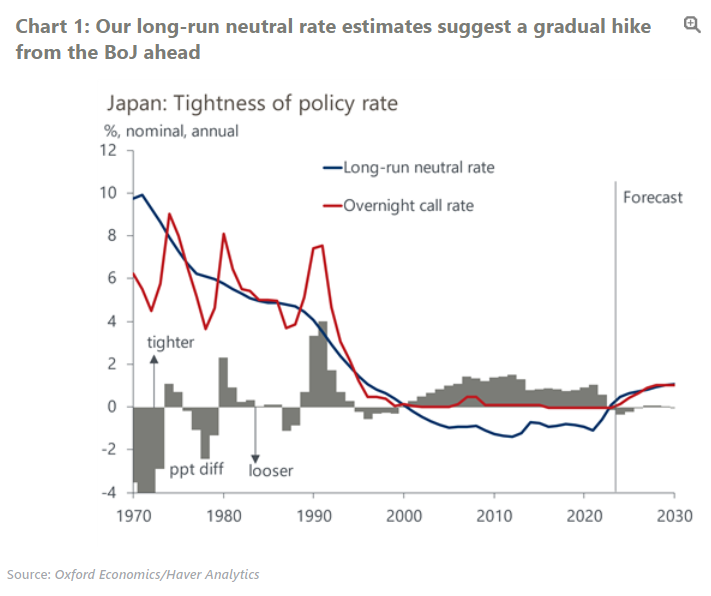

Japan’s neutral interest rate is rising, but not by much

We estimate that Japan’s nominal neutral interest rate – the rate consistent with monetary policy that is neither stimulative nor restrictive – has risen somewhat since 2022, marking a striking reversal from its decades-long slide. More importantly, we project it to continue rising gradually, to around 1% by 2030 from 0% in 2023.

What you will learn:

- Higher inflation expectations are one of the main reasons behind the recent increase in the nominal neutral rate. We believe that inflation expectations will continue to slowly edge up in the coming years amid robust wage gains, contributing to the projected neutral rate’s rise.

- Stripping out inflation expectations, the real neutral rate has risen only modestly in recent years. We think Japan’s demographic headwinds and weak productivity growth all but banish a sustained return to positive real neutral rates throughout our forecast to 2050. But in the next few years, increases in net foreign assets and the Bank of Japan’s step down in quantitative easing are likely to drive the rate slightly higher.

- Neutral rate estimates are inherently uncertain. Still, our approach provides a framework that can inform our view of the path for long-run interest rates, and our sensitivity and scenario analyses offer a useful gauge of the risks around our estimates.