Research Briefing

| Jun 14, 2024

Japan’s BoJ will start reducing JGB purchases in August

At Friday’s meeting, the Bank of Japan (BoJ) announced its decision to start reducing the volume of its JGB purchases by a substantial scale in August to ensure long-term rates are more market-oriented. At the next policy meeting on July 30th-31st, the bank will decide a detailed plan and schedule for the reduction covering the next two years after consulting with market participants.

What you will learn:

- As expected the BoJ decided to maintain its policy rate at 0%-0.1%. Wage growth looks set to remain robust based on the latest tally of the Spring Wage Negotiation, but household income and consumption are still weak and core-core CPI (excluding energy and fresh foods) eased further in April reflecting receding supply-side inflationary factors.

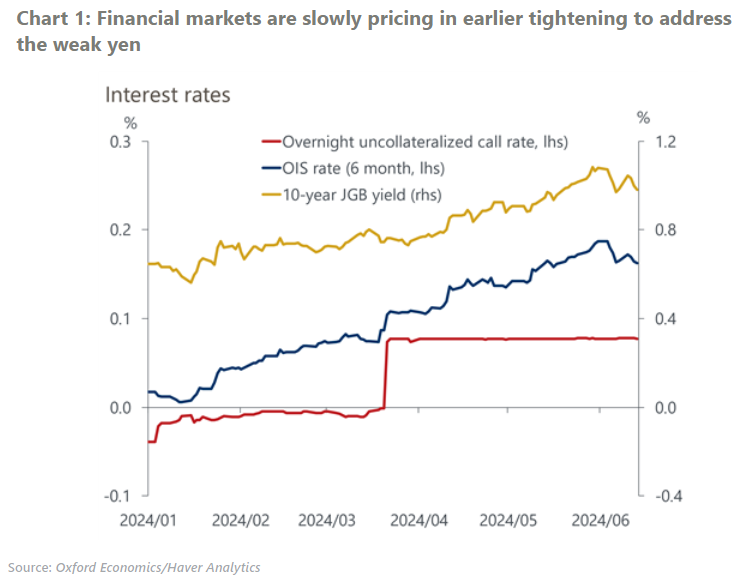

- Speculation over earlier tightening is rising in response to the weak yen. However, we believe the BoJ will wait until September to confirm that the strong wage settlement effectively raises real household incomes, and that consumption has gained momentum during the summer vacation.

- Despite recent hawkish statements by BoJ officials, we still think the yen weakness is unlikely to be a trigger for a rate hike. Most importantly, the BoJ’s rate hike will have only a limited impact on the currency which is dominated by the US monetary policy outlook.