Research Briefing

| Apr 28, 2023

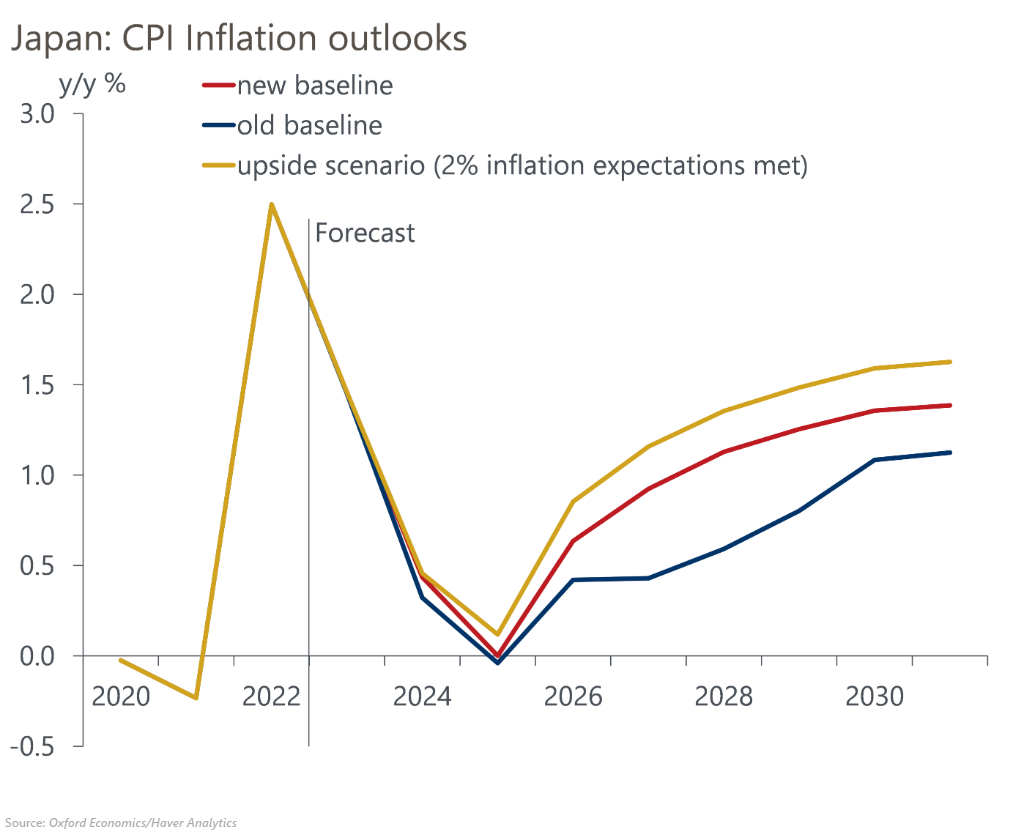

Japan: The impact of structural labour shortages on inflation

We have revised up our long-term wage and inflation projections based on a larger impact from structural labour shortages due to adverse demographic trends. Even after raising our wage growth assumptions by 0.5ppts on average over 2024-2030, however, we still forecast inflation only reaching 1.4% in 2030 – well short of the 2% target.

What you will learn:

- We now project higher base-wage increases for regular workers. We assume that wage growth set in the annual spring negotiations will rise gradually to 3% by 2030 from an average of 2.3% in the five years before the pandemic. Despite the rising need for wage increases to secure talented workers, Japan’s rigid employment system will constrain pay growth.

- We also revised up our projection for the hourly wage for part-time workers, which is more elastic to labour market conditions than wages for regular workers. We project hourly wages to increase as fast as in the late 2010s this year and then to accelerate, reaching close to 4% by 2030 due to the limited pool of additional labour supply.

- Gradual but persistent wage rises will boost inflation expectations accordingly. Given that Japan’s inflation expectations tend to be formed adaptively, we believe that inflation expectations will rise in accordance with actual price developments. In our baseline, we assume that inflation expectations will rise only gradually to 1.5% in 2030 from 1.1% in 2022.