Research Briefing

| Feb 27, 2024

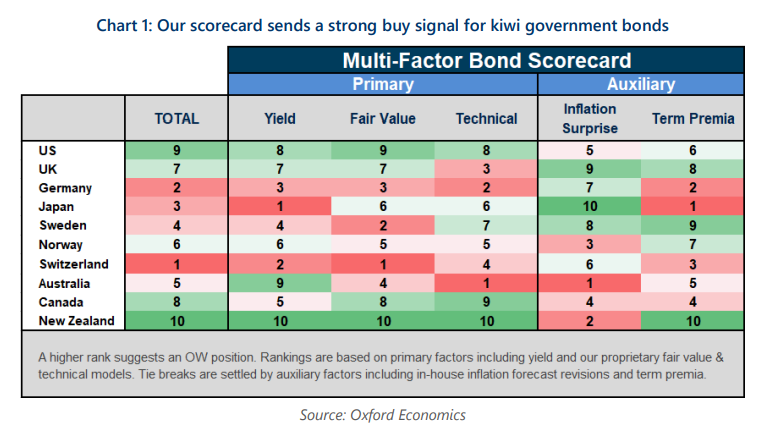

Fixed Income: Kiwi bonds to fly high

We remain steadfast on our long-standing heavy overweight in New Zealand government bonds within our global DM fixed income allocations.

What you will learn:

- Upside surprises in activity and inflation this year have opened the market’s mind to the possibility of a hike in H1. But we doubt the criteria set out in the November monetary policy statement for a hike have been met.

- Our economists think the RBNZ will instead remain on hold in H1 before cutting twice in H2 as inflation falls to target and unemployment rises.

- Our multi-factor rates scorecard adds to our conviction, sending a near unanimous signal that kiwi bonds will outperform other developed market govies in the near term, based on attractive term premia, cheap valuations and strong mean-reverting properties.

Related Reports

Click here to subscribe to our asset management newsletter and get reports delivered directly to your mailbox

Czech Republic: Profligate fiscal loosening will push up bond yields

We think the Czech 10-year bond yield is on track to breach 5% in the coming months, as the markets continue to price in the fiscally profligate programme of the new government.

Read more: Czech Republic: Profligate fiscal loosening will push up bond yields

Why bond yields are rising again and why it matters

The rise in bond yields reflects fiscal concerns, higher risk premia, shifting investor preferences, and idiosyncratic factors.

Read more: Why bond yields are rising again and why it matters

Indirect climate risk in financial analysis

Climate and other sustainability challenges can affect the finance sector and have a material impact on returns to capital.

Read more: Indirect climate risk in financial analysis

Economics for Asset Managers

Read more of our analysis and reports on asset management and economic outlook.

Read more: Economics for Asset Managers