Research Briefing

| Dec 7, 2023

Emerging Markets forecast issues – Policy easing faces stronger headwinds

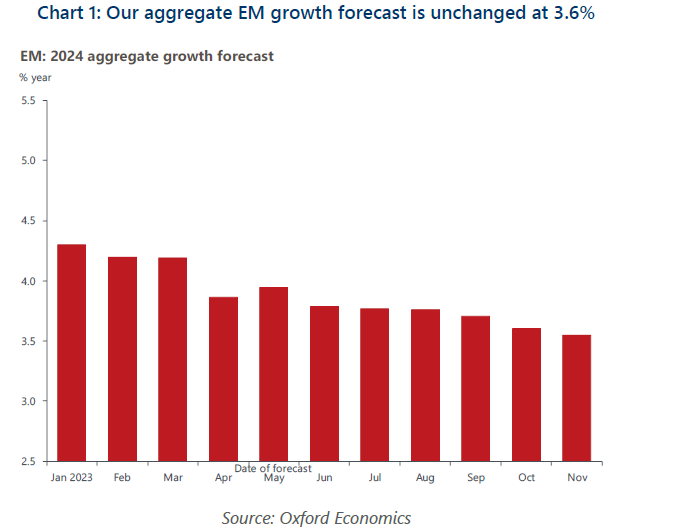

In our latest monthly forecast, we raised our aggregate 2023 GDP growth forecast for emerging markets (EMs) by 0.1ppt to 4.1%. We raised our 2023 GDP growth forecast for China by 0.1ppt to 5.2% after a slight outperformance in Q3, consistent with the official growth target of “around 5%”. We maintain our 2024 aggregate EM growth forecast at 3.6%.

What you will learn:

- Our aggregate EM average inflation forecasts are unchanged at 8.5% in 2023 and 7.6% in 2024, but we think country-specific inflation paths will diverge. Renewed food and energy price pressures may slow inflation’s decline in parts of EM Asia and Latin America. By contrast, we see disinflation progressing quicker in Central Europe amid falling demand.

- High US rates, a strong US dollar, and high oil prices led to surprise rate hikes in Indonesia and the Philippines, defying our predictions. In the Association of Southeast Asian Nations (ASEAN), the pivot to rate cuts is unlikely until Q2 2024, at the earliest. We raised our year-end policy rate forecasts across Latin America, with Mexico’s central bank first cut delayed until 2024.

- The extension of the pause in the Fed’s hiking cycle provides a reprieve to EM currencies and local bonds, somewhat improving the balance of risks assessed by EM central banks. We think the next move by central banks in 13 out of 20 major EMs will be a rate cut. But the surprise decision by Poland’s central bank to put its easing cycle on hold shows that even in Central Europe cuts may be delayed into 1H 2024.